Ever hit the open road on your bike and wondered what happens if a car cuts you off? You feel that thrill, but one crash could wipe you out without the right protection. That’s where motorcycle insurance steps in to save your wallet and peace of mind.

In this guide, you’ll discover everything about motorcycle insurance for 2026. We’ll cover how it works, what you need, and costs in states like Florida. You’ll get tips to find the cheapest options and avoid common traps. Stick with me, and you’ll ride smarter.

Most riders skip key details that cost them hundreds extra. You won’t make those mistakes. Let’s dive in and get your bike insurance sorted.

What Is Motorcycle Insurance Exactly?

Motorcycle insurance protects you if your bike gets damaged or you cause an accident. It covers repairs, medical bills, and legal fees. Think of it as your safety net on two wheels.

You pay a premium each month or year. In return, the insurer handles big claims. Without it, one wreck leaves you broke fast.

Here’s the thing: not all policies match every rider. Motorbike insurance works like car insurance but fits bikes better. Pick the wrong one, and you’re overpaying.

Why You Need Motorcycle Insurance in 2026

Riding without bike insurance risks fines, license loss, and huge bills. Most states demand at least liability coverage. You can’t legally ride without it in 49 states.

Crashes happen quick on bikes. Other drivers often don’t see you. Liability pays if you hurt someone else.

Pro Tip:

Skip motorcycle insurance, and a $20,000 accident bill lands on you. That’s no joke—over 80,000 bike crashes hit U.S. roads in 2024 (NHTSA, 2025).

It also covers theft. Bikes vanish fast from streets. Good coverage replaces yours quick.

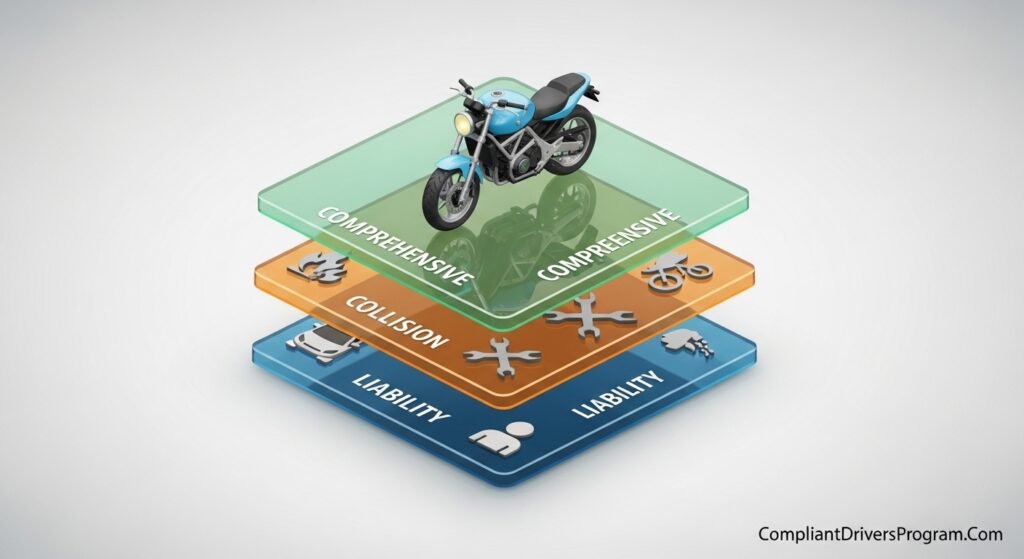

Coverage Types You Should Know

Coverage types vary by policy. Start with basics, then add extras. You pick what fits your ride and budget.

Liability covers damage you cause to others. It pays their repairs and medical costs. Most states require $25,000 per person minimum.

Collision fixes your bike after a crash. It doesn’t matter who’s at fault. Expect deductibles from $500 to $1,000.

Comprehensive handles theft, fire, or hail damage. Vandalism counts too. This shines for pricey custom bikes.

Don’t miss gear coverage. It replaces helmets and jackets up to $1,000 usually. Passenger coverage protects riders with you.

Curious about details? Check Collision Insurance Explained or Comprehensive Insurance.

Motorcycle Insurance for Beginners Explained

New to riding? Motorcycle insurance for beginners feels overwhelming at first. You worry about costs and what to pick. Relax—start simple.

Pick liability plus collision if your bike costs under $10,000. Add comprehensive for theft-prone areas. Agents help tailor it.

Most beginners overlook uninsured motorist coverage. It protects you from drivers without insurance. Over 13% of U.S. drivers skip it (IIABA, 2024).

Quick tip: Take a safety course. It drops your rates 10-15%. You’ll ride safer too.

How Motorcycle Insurance Works Step by Step

Wondering how does motorcycle insurance work? You buy a policy from a company. Pay your premium on time.

Something happens—like a crash. You file a claim online or by phone. They inspect damage and approve payout fast.

Adjusters visit your bike. They approve fixes or total it if costs exceed value. You get cash minus deductible.

Claims raise rates for 3-5 years. Drive safe to keep costs low. File smart—only for big issues.

State Rules: Do You Need Motorcycle Insurance in Florida?

Laws differ by state. Check Motorcycle Insurance Requirements by State for yours.

In Florida, do you have to have motorcycle insurance? Yes, but only $10,000 property damage liability. No bodily injury required. Is motorcycle insurance required in Florida? Absolutely—ride without it, and you face $150 fines plus suspension.

Florida motorcycle insurance averages $1,200 yearly. High theft and crashes drive it up. Compare quotes to beat the average.

California mandates $15,000 per person liability. Texas and Illinois follow suit at $30,000/$60,000. New York City (NYC) hits $1,800 average due to traffic.

Arizona (AZ), Utah, Georgia, Ohio, Massachusetts, Oregon, and Washington state all require minimums. SR22 filings boost costs for high-risk riders.

Special Types: Custom Motorcycle Insurance and More

Own a custom chopper? Custom motorcycle insurance covers mods like paint and parts. Standard policies skip them.

Motorcycle courier insurance adds business use. Deliver food or packages? You need it for extra liability.

Motorcycle breakdown insurance tows you if you stall. Costs $100−200 yearly. Pairs well with roadside help.

Temporary policies last 30 days. Great for test rides. Check Best Motorcycle Insurance Companies for options.

How Much Is Motorcycle Insurance? Real Costs

How much is insurance for a motorcycle? Averages $700−1,500 per year nationwide (Forbes, 2025). Beginners pay more—around $1,200.

Factors jack it up. Sport bikes cost 20% extra—see Sport Bike Insurance Rates. Age matters: under 25? Add $500.

Location hurts too. NYC riders pay $2,000+. Rural Georgia drops to $500.

Shop smart for cheapest. Multi-bike discounts save 15%. Bundling with car insurance cuts 25%.

Dive deeper at Motorcycle Insurance Cost.

Comparison Table: Coverage Options

| Option | Cost (Yearly Avg) | Best For | Effectiveness | Notes |

|---|---|---|---|---|

| Liability Only | $400-$800 | Budget riders | Medium | Meets state minimums; no bike repair |

| Liability + Collision | $800-$1,400 | New bikes | High | Covers crashes; add deductible |

| Full Coverage | $1,200-$2,500 | Custom/sports | Highest | All risks; includes gear (Source: III, 2025) |

| Custom Add-On | +$200-$600 | Modified bikes | High | Protects upgrades; check Cheap Motorcycle Insurance |

Tips to Lower Your Motorcycle Insurance Rates

Want the cheapest motorcycle insurance? Raise your deductible to $1,000. It drops premiums 20%.

Install anti-theft devices. Discounts hit 15%. Park in garages.

Quick tip: Compare 3+ companies. Use apps for instant quotes. Good credit saves 30% in most states.

Lay off the bike in winter. Suspend coverage to cut costs. Safety courses pay off big.

Avoid tickets. One speeding bust adds $300 yearly. Ride defensive.

Pro Tip:

Bundle with Cheap Car Insurance for 25% off both. See How to Lower Car Insurance Rates.

What to Avoid with Bike Insurance

Don’t buy minimum coverage only. It leaves your bike unprotected. One theft, and you’re out $10,000.

Skip shady online quotes. They hide fees. Stick to big names like Progressive or Geico.

Most people don’t know this: Gap insurance matters for new bikes. It covers the loan if totaled early.

Ignore SR22 if required. It proves high-risk coverage. Miss it, and your license stays gone.

External source: State laws from DMV.org (accessed 2026).

Unique Insights for 2026 Riders

Insight 1: Electric bikes get 10% discounts now. Batteries cost less to fix (Insurance Journal, 2025).

Insight 2: Telematics apps track safe riding. Save up to 40% with proof.

Insight 3: Passenger coverage saves lives—covers friends on back. Most skip it but crashes hit passengers hard (NHTSA, 2025).

Actionable: Get quotes today. Rates rise 8% in 2026 due to claims.

External source: Stats from NHTSA.gov (2025 report).

FAQ

A: Start with state minimum liability. Add collision and comprehensive for full protection. Tailor to your bike value.

A: File online, get inspected, receive payout minus deductible. Process takes 1-2 weeks usually.

A: Get liability plus safety course discount. Compare quotes from 3 companies for best rates.

A: Averages $60-125. Drops with clean record and discounts.

A: Yes, 49 states require it. New Hampshire is the exception with proof of funds.

A: Yes, at least $10,000 property damage. Fines hit without it.

A: Yes, even mopeds over 50cc. Check local DMV for details.

Ready to Ride Protected?

- Grab state minimum liability to stay legal, then add collision for bike fixes.

- Shop quotes for cheapest rates—aim 20% under average.

- Use discounts like safety courses and bundling to save hundreds.

- Check custom needs and states like Florida for specifics.

Your next step? Head to a quote tool now. Enter your zip and bike details. You’ll lock in coverage today and hit the road worry-free.

Motorcycle Insurance Calculator

Get Your Estimated Premium in Seconds • 2026 Updated Rates

✅ Your Estimated Premium

- Take a safety course to save 10-15%

- Install anti-theft device for extra discount

- Bundle with car insurance for 25% off

This article is for information only. Please consult a professional before making decisions.

Leave a Reply