Maybe you backed into a pole in a tight parking spot, or slid into a guardrail on a slick road. That instant sinking feeling? That’s where Collision Insurance steps in to save the day. It pays to repair your vehicle, even if the mistake was yours.

Let’s cut through the noise. This guide strips away the fine print to explain Collision Coverage in simple language. From 2026 pricing trends to the big question—’Do I really need this?’—we’re giving you the facts without the headache.

What Is Collision Insurance?

Let’s keep this easy: Collision insurance pays to fix or replace your car if it’s damaged in an accident while you’re driving.

It covers accidents like:

- You collide with another car.

- You hit a stationary object like a wall, tree, or fence.

- Your car flips over after hitting something.

It doesn’t matter who caused the crash — this coverage still helps. Once you pay your deductible, your insurance company covers the rest (up to your car’s value).

Example:

You hit a light pole, and repairs cost $4,000. If your deductible is $500, insurance pays the remaining $3,500.

This simple protection can save you thousands when accidents happen — and in 2026, repair costs keep climbing due to expensive technology in modern cars.

Why You Might Need Collision Insurance in 2026

Car repairs are not what they used to be. Even a small accident can drain your wallet.

In 2026:

- Bumper repairs can cost $1,800–$2,500

- Windshield sensors can cost $400–$900

- Headlight replacements can be $1,000+ for newer models

That’s why collision coverage is more important than ever. It fills the gap between your savings and a big repair bill.

Pro Tip: Even careful drivers get hit. One distracted text or slippery turn can do serious damage. Collision insurance keeps that one bad day from wrecking your finances.

Collision Insurance vs Comprehensive Insurance

These two coverages often get mixed up, so here’s the quick difference:

| Coverage Type | What It Covers | Example | Average Cost (2026) |

|---|---|---|---|

| Collision Insurance | Accidents where your car hits something | You rear-end another car | $350–$650 per year |

| Comprehensive Insurance | Non-accident events like theft, fire, or weather damage | A tree branch falls on your car | $180–$400 per year |

In short:

- Collision = crash damage while driving

- Comprehensive = things that happen when you’re not driving

Drivers often combine both for “full coverage.” Read more details about Comprehensive Insurance if you’re thinking about pairing them.

How Collision Coverage Works (Step-by-Step)

Here’s what actually happens after you crash your car:

- Stay safe first. Move to a safe place, check for injuries, and call for help if needed.

- Report the accident. Notify your insurer as soon as you can (many have mobile apps now).

- Take photos. Capture your car’s damage and any objects hit.

- Estimate damage. Your insurer will send an adjuster or ask for pictures to assess repair costs.

- Pay your deductible. This is your out-of-pocket part before insurance pays.

- Get your car fixed. Choose your repair shop, and the insurer covers the rest.

Example: If repairs total $5,000 and your deductible is $1,000, the insurance company pays $4,000.

Many insurers now use digital claim systems powered by AI, so payouts can happen within 3–5 business days instead of waiting weeks.

What Collision Insurance Doesn’t Cover

Collision insurance protects your car, but not everything related to an accident.

It doesn’t cover:

- Injuries to people (you’ll need Personal Injury Protection)

- Damage to someone else’s car (that’s Liability Insurance Car)

- Theft, floods, or weather damage (that’s comprehensive).

- Routine repairs like tires, oil changes, or mechanical issues.

To stay fully protected, you’ll want to combine these coverages — sometimes called full coverage car insurance. You can explore how that works in Full Coverage Car Insurance.

Cost of Collision Insurance in 2026

Rates vary, but here’s what most drivers are paying in 2026:

| Vehicle Type | Average Yearly Cost |

|---|---|

| Compact car | $330–$480 |

| SUV | $420–$600 |

| Pickup truck | $500–$700 |

| Luxury car | $620–$1,100 |

| Electric vehicle | $800–$1,400 |

Your cost depends on things like your location, driving history, and deductible. States with higher traffic or accident rates (like California and Texas) tend to have higher premiums than smaller towns.

Pro Tip: Ask your insurer for “low mileage” or “safe driver” discounts. In 2026, you can save 10–20% by installing a tracking app that shows good driving habits.

You can also check realistic averages at Average Car Insurance Cost.

Is Collision Insurance Worth It?

This depends on your car’s age and value.

If your car is new or still has a loan, having collision coverage is almost always worth it. New cars cost far more to fix — and a totaled car without coverage can leave you with debt.

But if your car’s older (say 10+ years) and worth less than $3,000, it might not make sense. The premium plus deductible could be more than what your car’s worth.

Example:

Your 2014 car is worth $2,500. You pay $400 yearly for collision and have a $500 deductible. That’s $900 total — almost half your car’s value.

In that case, you might drop it and start saving that money for future repairs.

Quick Tip: Use websites like Kelley Blue Book or Edmunds to check your car’s current value before deciding.

What If You Have a Collision Without Insurance?

Here’s the reality: without collision coverage, you’re on your own.

A small crash could cost anywhere from $2,000 to $8,000 in 2026. If the other driver is uninsured or refuses to pay, you’ll still need to cover the repairs.

That’s why many drivers also get Uninsured Motorist Coverage. It helps you if the other driver doesn’t have the right insurance.

Without collisions or uninsured driver coverage, even minor accidents can snowball into major expenses.

How to Negotiate a Better Collision Claim

Not many people know this, but you can negotiate your insurance payout.

Here’s how to make that work:

- Collect 2–3 repair estimates from local shops.

- Compare them to the insurer’s estimate.

- Show your car’s market value from Kelley Blue Book or Edmunds.

- Stay calm and polite. Explain why your estimate is more accurate.

If your car is declared “totaled,” ask if the insurer can add taxes and registration fees to the payout — many companies do if you ask politely.

According to the National Association of Insurance Commissioners (2025), people who provide written evidence get up to 25% more in claim settlements.

Motorcycle and Electric Vehicle Coverage

If you drive a motorcycle or electric car, collision coverage works the same way — but costs vary.

- Motorcycle collision coverage: $250–$460/year

- EV collision coverage: $700–$1,400/year

EVs usually cost more because of their expensive sensors and battery systems. But some insurers now offer “green car discounts” to help offset those high rates.

Pro Tip: Bundle your home, motorcycle, and car insurance with the same company to save another 10–20%.

The Deductible: Picking the Right One

Your deductible is what you’ll pay after an accident before your insurance kicks in.

Here’s how to choose the right amount:

- Low deductible ($250–$500):

Higher monthly payment, but less out-of-pocket if you crash. - High deductible ($1,000+):

Cheaper monthly bill, but more to pay at repair time.

Most drivers in 2026 choose about $750 — it keeps premiums manageable without huge risk.

Example:

If your deductible jumps from $500 to $1,000 and saves $25 a month, you’ll save $300 a year — but make sure you have $1,000 easily available.

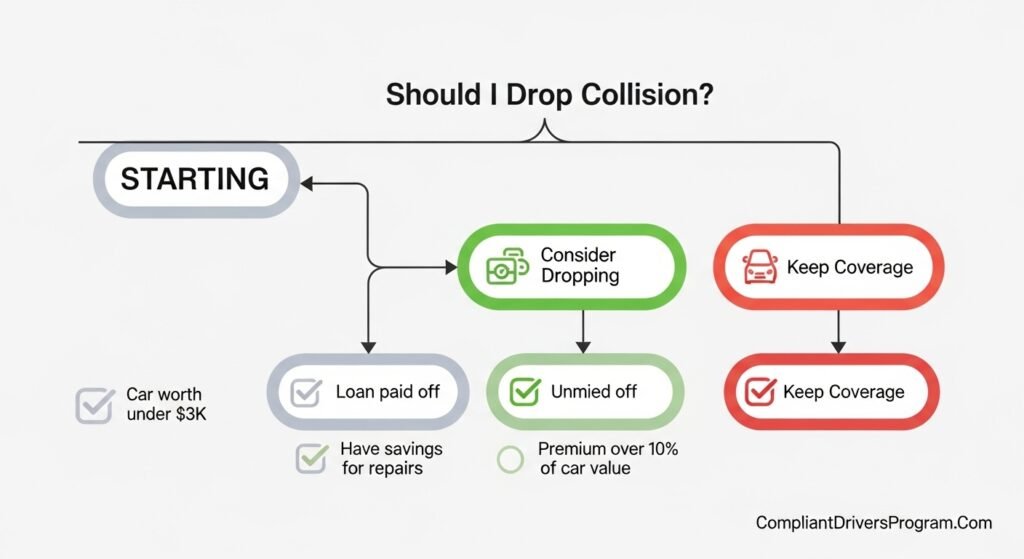

When Should You Drop Collision Coverage?

You might consider dropping collision insurance if:

- Your car’s value is below $3,000.

- You’ve paid off your loan or lease.

- You have enough savings to cover repairs yourself.

- Your yearly premium is more than 10% of your car’s total value.

But keep it if your car is newer, you commute daily, or you’d struggle to pay for sudden repairs.

If you owe more than what your car’s worth, add Gap Insurance. It covers the difference if your car gets totaled and you still owe money on your loan.

FAQs About Collision Insurance

A: It covers your car’s repairs when you hit another car or object while driving.

A: Collision covers crashes; comprehensive covers theft, weather, or vandalism.

A: If your car’s worth less than $3,000, it may be cheaper to drop it.

A: No, but lenders or leasing companies often require it.

A: Between $30 and $55 a month, depending on your car and location.

A: Yes, usually if the other driver can’t be identified.

A: Yes — most policies cover your car, no matter who’s driving (with permission).

Final Thoughts

Here’s what matters most:

- Collision insurance saves you from huge bills after a crash.

- Repairs in 2026 are more expensive than ever.

- Pair collision with comprehensive and liability insurance for complete protection.

- Recheck your car’s value every year to see if keeping it still makes sense.

If you’re unsure, talk to your agent or compare quotes from multiple companies — you might be able to lower your premium without losing coverage.

This article is for information purposes only. Please speak with a licensed insurance expert before making policy changes.

🚗 Collision Coverage Calculator

Smart 2026 collision insurance analysis tool

⚠️ Estimates only. Consult a licensed insurance professional.

Leave a Reply