Here’s a common question drivers still ask in 2026 — “If I crash my car, does liability insurance cover it?” It’s one of those confusing topics where people spend years paying for coverage they don’t fully understand.

Here’s the truth: Liability Insurance Car is like a safety net, but it protects other people, not you. It saves you from paying high bills when you cause an accident, but it won’t replace or repair your own vehicle.

This guide breaks it all down — what’s covered, what’s not, new 2026 insurance rules, real examples, and how to choose the right coverage for your budget. By the end, you’ll know exactly how to make smart insurance decisions that protect your money and your peace of mind.

What Is Liability Insurance Car?

Let’s start simple. Liability Insurance Car is a type of auto insurance that covers costs if you’re at fault in an accident that damages someone else’s car or injures other people. It doesn’t pay to repair or replace your car.

It’s made up of two core parts:

- Bodily Injury Liability (BI): Covers medical costs, rehabilitation, and lost income for other people injured in an accident you cause.

- Property Damage Liability (PD): Pays for repairing or replacing another person’s vehicle or property damaged in the accident.

Every U.S. state (except New Hampshire) requires drivers to carry auto liability insurance as the minimum legal coverage. States like California and Texas have specific minimum required limits — for example, 30/60/25 in Texas.

Learn more about your state’s rules in Minimum Car Insurance Requirements.

Quick Tip: Always carry more than the minimum. It’s cheap protection compared to the cost of one serious crash.

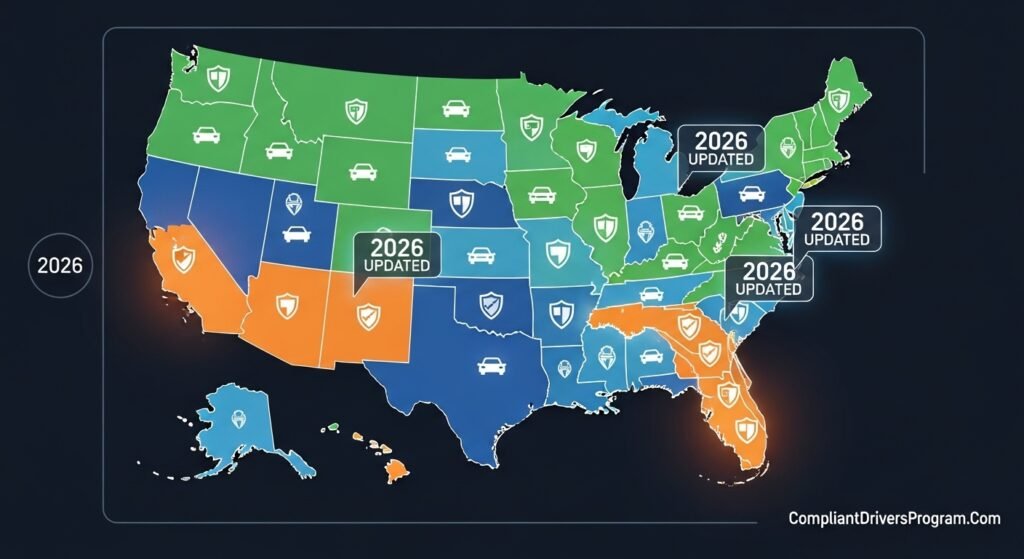

Updated 2026 State Laws and Limits

As of 2026, several states updated their minimum liability coverage limits to reflect rising repair and medical costs.

- California (2026): Minimum increased to 30/60/25 from 15/30/5.

- Florida (2026): New law requires all drivers to carry bodily injury liability (BI), previously optional.

- Texas: Still 30/60/25, but proposals aim for 50/100/50 by 2028.

These changes came after inflation raised the average cost of a single-car accident injury to over $25,000 (National Highway Traffic Safety Administration, 2025).

If your policy hasn’t been updated in years, check your limits — your coverage might be too low for today’s repair and hospital costs.

Why Liability Coverage Still Matters in 2026

Despite more tech in cars and rising costs, liability insurance remains the one coverage every driver needs.

Why? Because one bad accident can drain your savings and damage your future.

Imagine this: you hit an electric SUV worth $85,000, injure two people, and total both cars. Without liability coverage, you’d owe hundreds of thousands out-of-pocket.

But with liability coverage, your insurer covers the bills up to your policy limit, saving your bank account.

Pro Tip: In 2026, the average accident claim with injuries costs over $27,800, while a property damage claim averages $5,400 (Insurance Information Institute, 2025).

What Exactly Does Liability Insurance Cover?

When you pay for Liability Insurance Car, here’s what you’re really getting for your money:

1. Medical Bills for Others (Bodily Injury Liability):

Covers emergency care, follow-up visits, hospital stays, and rehabilitation for people you injure in an accident.

2. Property Damage to Others (Property Damage Liability):

Pays for repairs to vehicles, buildings, fences, or other property damaged by your car.

3. Legal Fees:

If someone sues you after an accident, your insurer covers lawyer costs and settlements up to your policy limit.

4. Funeral Costs:

In serious accidents, your BI coverage may help with funeral expenses for others who lose their lives in the crash.

5. Court Settlements:

Covers payments awarded by courts if you’re found liable in a lawsuit.

All this protection helps you avoid financial disaster — but again, it only applies to others, not your car or medical bills.

What’s Not Covered by Liability Insurance

Here’s the honest part most drivers forget: Liability Insurance Car doesn’t pay for everything.

You’re on your own for:

- Damage to your own car (even if you caused the crash)

- Theft, vandalism, or fire damage

- Natural disasters, flooding, or hail

- Hitting animals on the road

- Your medical bills or those of your passengers

For these gaps, you’ll want:

- Collision Insurance to protect your car in an accident.

- Comprehensive Insurance for theft, weather, or other non-collision damage.

- Personal Injury Protection for your medical expenses.

Pro Tip: Combine liability, comprehensive, and collision for “full coverage” — it’s what protects both you and others.

Does Liability Insurance Cover My Car If Someone Hits Me?

No — liability doesn’t cover your car if someone else crashes into you. The at-fault driver’s insurance should pay for your repairs. But if that driver doesn’t have insurance or drives away, you’re stuck.

To protect yourself, add Uninsured Motorist Coverage, which pays for your damages even if the other driver has no insurance. See Uninsured Motorist Coverage for details.

Does Liability Insurance Cover Car Theft or a Stolen Car?

No again. Liability has zero protection for stolen or vandalized vehicles.

If your car gets stolen, the only coverage that helps is Comprehensive Insurance. It covers crimes, natural events, and even windshield damage.

So, if you’ve wondered — “Does liability insurance cover stolen car?” — the answer in 2026 is still no.

Does Liability Insurance Cover My Car If I Hit Someone?

If you hit someone else, liability insurance covers them, not you.

- Their medical bills? Covered.

- Their car repairs? Covered.

- Your car repairs? Not covered.

You’ll need collision insurance to repair your vehicle. It’s the most common add-on for drivers who want to avoid paying thousands out-of-pocket after an at-fault crash.

Learn more about the difference in Full Coverage Car Insurance.

Liability Insurance for Lawn Care and Other Small Businesses

Here’s an angle most drivers forget: liability insurance isn’t just for cars. It’s also key for small business owners, especially those in service jobs like lawn care, construction, or cleaning.

Liability insurance for lawn care business covers damages if your workers accidentally break a client’s property or cause injuries while working.

Just like car insurance, it protects others from your business mistakes — not your tools or vehicles. So, always pair it with equipment coverage for full protection.

How Much Liability Insurance Should You Have in 2026?

Basic state limits aren’t enough anymore. Prices for parts and hospital care skyrocketed since 2023.

For peace of mind, go beyond the minimum. Experts now recommend:

- Bodily Injury Liability: $100,000 per person / $300,000 per accident

- Property Damage Liability: $100,000 minimum

- Umbrella Policy (optional): Adds extra coverage beyond liability limits

Pro Tip: The cost difference between minimum coverage and strong coverage is often just $15–$25 more per month.

If you’re wealthy, own a home, or have savings, those limits will protect your assets if a major lawsuit hits.

Average Cost of Liability Insurance in 2026

Insurance rates in 2026 increased slightly due to higher vehicle repair and medical costs. Based on 2025–2026 data from Bankrate and the Insurance Information Institute:

- Average monthly cost: $72

- Average annual cost: About $860

- Cheapest states: Maine, Ohio, and Vermont

- Most expensive states: Florida, Nevada, and California

If you’re looking to save, check Cheap Car Insurance for practical ways to lower rates through good driving habits, usage-based insurance, and discounts.

Can You Have Liability Insurance on a Financed Car?

Technically yes, but most lenders won’t allow it.

If your car is financed, the bank or leasing company will require full coverage, including comprehensive and collision. That ensures the vehicle — which they technically own — stays protected.

If you cancel full coverage, they might add force-placed insurance to your loan, which costs 2–3 times more.

For financed cars, 2026 drivers often add Gap Insurance. It pays the remaining loan balance if your car is totaled but worth less than what you owe.

My Car Is Totaled and I Only Have Liability Insurance — What Now?

Unfortunately, liability-only won’t help. If your car is totaled and you’re at fault, you’ll have to pay for replacement yourself.

This is where drivers often regret buying the cheapest policy. It might save $40 a month but cost thousands later.

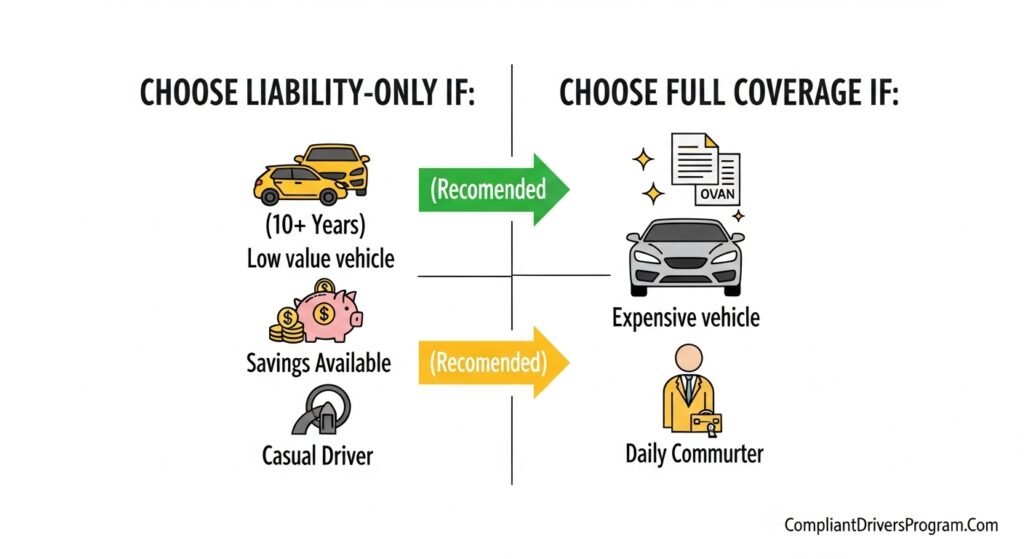

If your car is older (10+ years) or worth under $4,000, liability-only might make sense. But for newer vehicles or daily drivers, full coverage is the smarter move.

Real Example: Steve’s 2026 Accident Story

Here’s a real scenario that explains how liability works:

Steve, a Texas driver, rear-ends a Tesla in 2026. The Tesla needs $14,000 in repairs, and the other driver suffers minor injuries costing $9,000 in medical bills.

Steve’s liability coverage limit is 50/100/25. That means his insurance covers everything — but if it had been the older 30/60/25 limit, he would’ve owed the extra $- based on over-limit costs.

Moral of the story? Update your coverage as car repair prices rise.

When Liability-Only Makes Sense in 2026

Stick with liability-only car insurance if:

- Your car’s value is under $5,000.

- You have savings to replace it if needed.

- You drive infrequently or use public transport often.

- You live in a low-risk area.

Otherwise, pair it with Comprehensive Insurance or Collision Insurance for full peace of mind.

Comparison: Liability vs. Full Coverage (Updated for 2026)

| Type | Monthly Cost (2026 Avg) | Covers Your Car | Covers Others | Best For |

|---|---|---|---|---|

| Liability Only | $60–$90 | ❌ No | ✅ Yes | Older, paid-off, or cheap cars |

| Full Coverage | $130–$210 | ✅ Yes | ✅ Yes | New, leased, or financed cars |

| Liability + UM | $85–$115 | ✅ Partial | ✅ Yes | Drivers in states with many uninsured drivers |

FAQs – 2026 Edition

A: It covers injury and property damage you cause to others when you’re at fault.

A: No. The other driver’s insurance should pay, or you’ll need uninsured motorist coverage.

A: No. Theft, vandalism, or fire are covered under comprehensive insurance.

A: Not recommended — lenders require full coverage for financed vehicles.

A: Aim for at least 100/300/100, or get an umbrella policy for extra protection.

A: You’ll have to pay for your own car’s replacement or repairs.

A: It usually extends to rentals you drive for personal use within the U.S.

Key Takeaways and Next Step

- Liability Insurance Car protects you from paying for damage you cause to others.

- It’s required in almost every state in 2026.

- It doesn’t cover your car, theft, or weather damage.

- Carry higher limits to avoid lawsuits or big bills.

- Combine with collision, comprehensive, or uninsured motorist coverage for full protection.

The smartest move for 2026? Review your auto policy this year. With repair costs at all-time highs, increasing your liability coverage is one of the simplest, cheapest ways to secure your future on the road.

This article is for information only. Please consult a licensed insurance professional before making financial decisions.

🚗 Liability Coverage Calculator

Find Your Ideal Auto Insurance Coverage for 2026

✓ Updated with 2026 State LawsUpdated for 2026 state laws and requirements.

Leave a Reply