Have you been told you need SR-22 Insurance and now you feel stressed and confused? You’re not alone, and you’re not the first driver to feel lost after a DUI, accident, or license suspension.

Here’s the thing: an SR-22 doesn’t have to ruin your life or your budget. Once you understand what it means, how to file it, and how to keep costs low, you can get back on the road and rebuild your record step by step.

In this 2026 guide, you’ll learn what SR-22 insurance really means, how SR22 filing works, what SR-22 insurance coverage includes, how much SR-22 insurance cost you can expect, and how rules differ by state like California, Florida, Illinois, Ohio, and Indiana. You’ll also see special options like non owners SR-22, cheaper rates, and smart ways to get a second chance.

Quick tip: Grab a notebook or notes app while you read. You’ll see clear action steps you can follow today.

SR-22 Insurance Meaning: Simple Definition

Most people don’t know this, but SR-22 Insurance is not actually a type of insurance policy. It’s a financial responsibility form your insurer files to prove you carry at least the state minimum liability coverage.

The SR-22 form or SR-22 certificate shows your state that you’re insured after a serious driving problem. It’s filed with your DMV or similar agency and “attaches” to your auto policy so the state can monitor you.

So when you hear “define SR-22 insurance,” the easiest meaning is this: it’s proof that a high risk driver now has the required coverage and is being watched for lapses.

When the State Requires SR-22

Here’s the thing: states don’t ask for SR22 filing for small mistakes like a single parking ticket. They reserve it for bigger issues that suggest more risk.

You may need SR-22 Insurance if you:

- Got a DUI or DWI (one of the most common reasons).

- Drove with a suspended license or had your license revoked.

- Drove without insurance, especially more than once.

- Caused an at-fault accident while uninsured.

- Collected too many traffic violations in a short time (reckless driving, extreme speeding, street racing).

Some states may even require SR-22 for certain court-related issues not directly tied to driving, but that’s less common.

Pro Tip: The letter from the court or DMV usually tells you exactly which form you need: SR-22, FR-44 (in some states like Florida and Virginia), or another financial responsibility form.

What SR-22 Insurance Coverage Includes

Most people ask, “what is SR 22 insurance coverage?” The answer is surprisingly simple: it just proves you meet your minimum liability insurance limits. The form itself doesn’t add extra protection.

Your SR-22 policy usually includes at least:

- Bodily injury liability – Covers injuries to others when you’re at fault, up to your limit.

- Property damage liability – Covers damage you cause to other cars or property.

The SR-22 certificate doesn’t change things like collision or comprehensive. If you want protection for your own car, you still need options like Collision Insurance Explained and Comprehensive Insurance.

Most people don’t know this: The SR-22 form doesn’t control your coverage types. It only reports to the state that your liability coverage meets or exceeds the legal minimum.

Step-by-Step: How to Get SR-22 Insurance

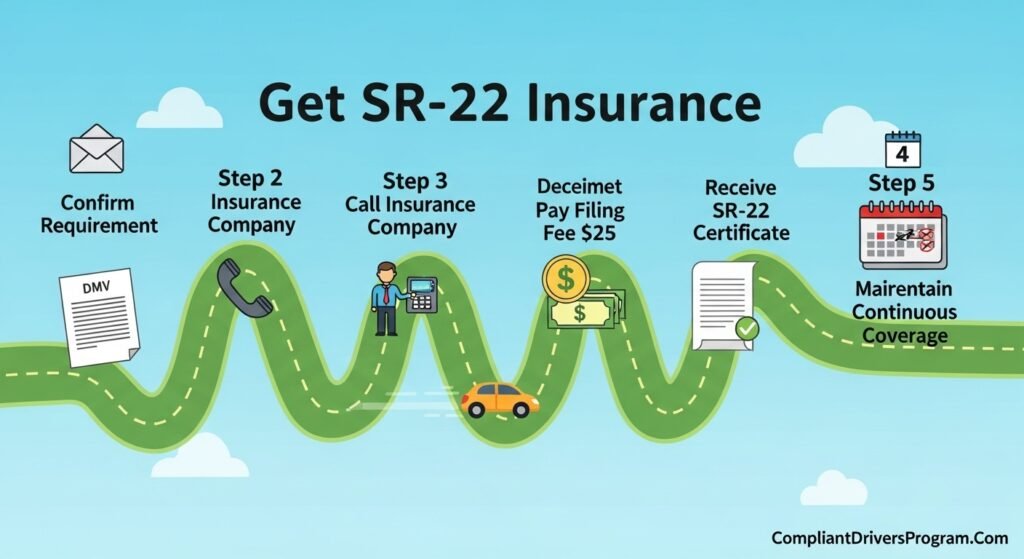

If you’re wondering how to get SR-22 Insurance, here’s your clear step-by-step roadmap:

Step 1: Confirm the Requirement

First, look at your court order or DMV notice. Check:

- Do they ask for SR-22, FR-44, or another form?

- How long must you keep it on file?

- Is it tied to a DUI, accident, or another violation?

Your state DMV or an official site like USA.gov motor vehicle services can also explain local rules.

Step 2: Call Your Current Insurance Company

Tell your agent, “I need an SR-22 filing added to my policy.” Many major insurers can file it electronically within 24–72 hours.

But here’s the catch: some companies don’t work with high risk drivers and may cancel or non-renew your policy instead. In that case, you’ll need to shop for Second Chance Auto Insurance or High Risk Auto Insurance.

Step 3: Pay the SR-22 Filing Fee

There’s usually a one-time filing fee around $15–$35, with $25 being the most common amount. This is added to your premium, not paid to the DMV by you directly.

Step 4: Wait for the SR-22 Certificate

Your insurer sends the SR-22 form to the state electronically. Once accepted, they can give you a copy of your SR-22 certificate for your records or to show the court if needed.

Step 5: Keep Continuous Coverage

Here’s the most important rule: do not let your policy lapse. If you cancel, miss payments, or switch companies without a new SR-22 in place, your insurer must notify the state, and your license can be suspended again.

Pro Tip: When changing companies, overlap your old and new policies by a few days to avoid any gap in financial responsibility reporting.

SR-22 Insurance Cost in 2026

Now let’s talk about SR 22 insurance cost, because that’s what usually scares people.

According to recent data, drivers who need an SR-22 pay much more than drivers with clean records. One major study found average SR-22 drivers pay around $256 per month or about $3,078 per year, though this varies widely by state and violation. Another 2024–2025 analysis found average costs near $3,295 per year for drivers with a DUI-related SR-22.

On top of higher premiums, you’ll usually pay:

- Filing fee: about $25 once.

- Possible reinstatement fees to the DMV.

- Court fines from the original offense.

So SR-22 itself isn’t expensive. The high risk label is what raises your long-term costs.

Fresh 2026 SR-22 Cost Snapshot by State

Recent 2025–2026 pricing trends show big differences between states. Here’s a helpful table using approximate ranges to give you a realistic idea for high risk SR-22 drivers with a serious violation like DUI or driving uninsured:

For a deeper cost breakdown across states, you can compare updated numbers at SR-22 Insurance Cost by State.

Unique insight: Many people assume big-name companies are always more expensive for SR-22, but in some rural areas they can actually be cheaper than small regional insurers. Always get at least 3–5 quotes.

SR-22 Insurance Requirements by State

SR-22 insurance requirements by state can change slightly, but most follow the same basic pattern: keep proof of financial responsibility for 1–5 years, usually 3.

Here are some key 2026 highlights:

- California

- Typical term: 3 years after DUI or major violation.

- Canceling or letting your policy lapse triggers a fresh suspension.

- Florida

- Illinois

- Ohio

- Indiana

You can always double-check state-specific rules at official DMV pages linked through USA.gov.

Non Owners SR-22 Insurance: Driving Without a Car

What if you don’t own a car but still need to drive sometimes? That’s where non owners SR-22 insurance comes in.

According to major insurers, a non-owner SR-22 is designed for drivers who must file an SR-22 but don’t own a vehicle. You buy a non owner car insurance policy, and the company files the SR-22 form tied to you, not to a specific car.

Key points about non-owner SR-22:

- It provides liability coverage only when you drive cars you don’t own.

- It usually meets just the minimum state requirements, making it cheaper than full coverage.

- It’s great for keeping your license valid while you drive rentals, work vehicles, or borrowed cars.

One helpful detail most people miss: non-owner SR-22 is usually secondary coverage. If you borrow a friend’s car and crash, their policy pays first, and your non-owner policy only helps if their limits are exhausted.

For a deeper look at how non-owner policies work, you can read more at Non Owner Car Insurance.

High Risk Drivers: SR-22 After DUI or Bad Record

If you’re dealing with Insurance After DUI or need Insurance for Bad Driving Record, you’re in the high risk category. That’s exactly where SR-22 Insurance shows up.

Drivers may need SR-22 after:

- A DUI or DWI conviction.

- Several speeding tickets or reckless driving charges.

- A serious accident where you were at fault and uninsured.

For DUI-related SR-22, average yearly premiums can climb above $3,000, and sometimes over $4,000 in states with strict laws.

To soften the impact, look into:

- Insurance After DUI for carriers that work with DUI drivers.

- Insurance for Bad Driving Record for tailored high risk auto insurance options.

- Second Chance Auto Insurance for companies that specialize in drivers starting over.

Pro Tip: Enroll in a certified defensive driving or DUI education program where allowed. Some insurers will offer a small discount once you complete the course, even with an SR-22.

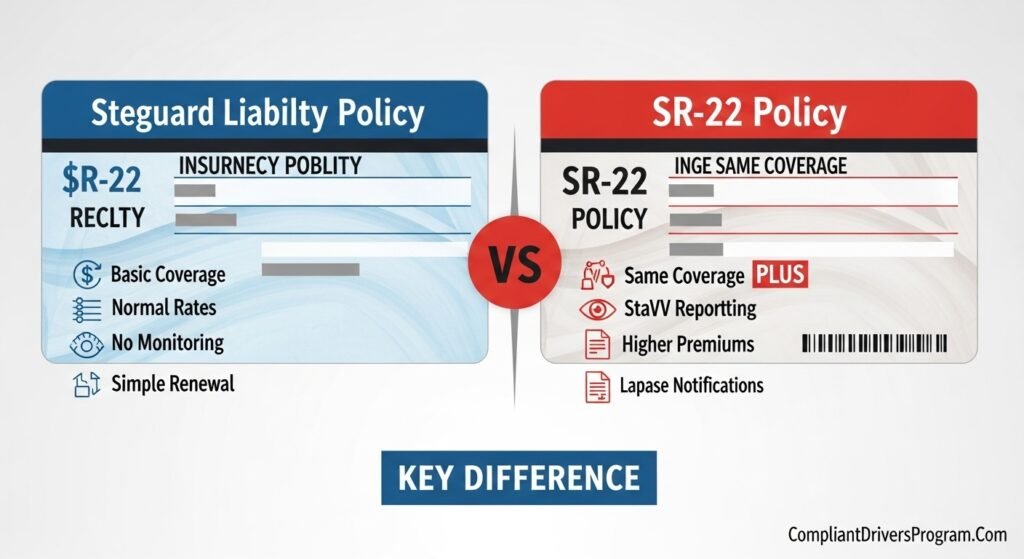

SR-22 vs Regular Liability Insurance

Most people wonder how SR-22 Insurance compares with regular Liability Insurance Car coverage. Here’s a clear view:

| Feature | Regular Liability Policy | Policy with SR-22 |

|---|---|---|

| Purpose | Financial protection if you cause harm | Prove financial responsibility to the state |

| Who Needs It | Most drivers | High risk drivers only |

| Cost | Based on age, car, record | Higher due to violation and risk |

| Form Filed | None | SR-22 form or similar |

| Monitoring | No reporting to DMV | Insurer must report lapses |

Your coverage types can be the same under both. The big difference is that SR-22 adds a legal state requirement and extra oversight.

If you only want to meet minimum car insurance requirements with SR-22, see Minimum Car Insurance Requirements to understand basic limits.

How Long Do You Need SR-22?

Most people keep SR-22 Insurance for three years, but in some states it can range from one to five years depending on the offense.

Here’s what usually affects the time period:

- Type of violation (DUI often means longer terms).

- Whether it was your first or repeated offense.

- State-specific law and court order.

Important: the clock only runs while your SR-22 policy is active. If your coverage stops and your insurer files a cancellation, your state can pause or reset your required SR-22 period.

Tips to Lower SR-22 Insurance Cost in 2026

You can’t erase a DUI or suspension overnight, but you can still control your SR 22 insurance cost. Use these smart 2026 strategies:

- Compare multiple quotes. Insurify’s 2026 research shows major price differences between companies, even for the same driver.

- Choose a cheaper car. Older, modest vehicles are cheaper to insure than sports cars or luxury models.

- Raise your deductibles. If you carry collision or comprehensive, higher deductibles usually mean lower premiums.

- Take a safe driving course. Some insurers offer discounts for completing an approved course, even for high-risk drivers.

- Drive less. Low mileage often qualifies for small discounts and reduces chances of new violations.

Also consider moving toward more basic coverage if your car is older and paid off, but never drop below your state requirement or what your lender requires.

Common Mistakes to Avoid with SR-22

Here’s what many drivers get wrong — and you can avoid easily:

- Forgetting to pay on time. A missed payment can cause a cancellation and a fresh suspension notice.

- Switching insurers without overlap. Even a one-day gap can cause a compliance issue.

- Not confirming the end date. Always verify with the DMV when your SR-22 requirement is truly over.

- Assuming SR-22 covers everything. Remember, it’s only proof of liability, not full coverage.

Pro Tip: Set automatic payments and calendar reminders each month. Treat your SR-22 period like a probation phase you must finish clean.

FAQ: SR-22 Insurance 2026

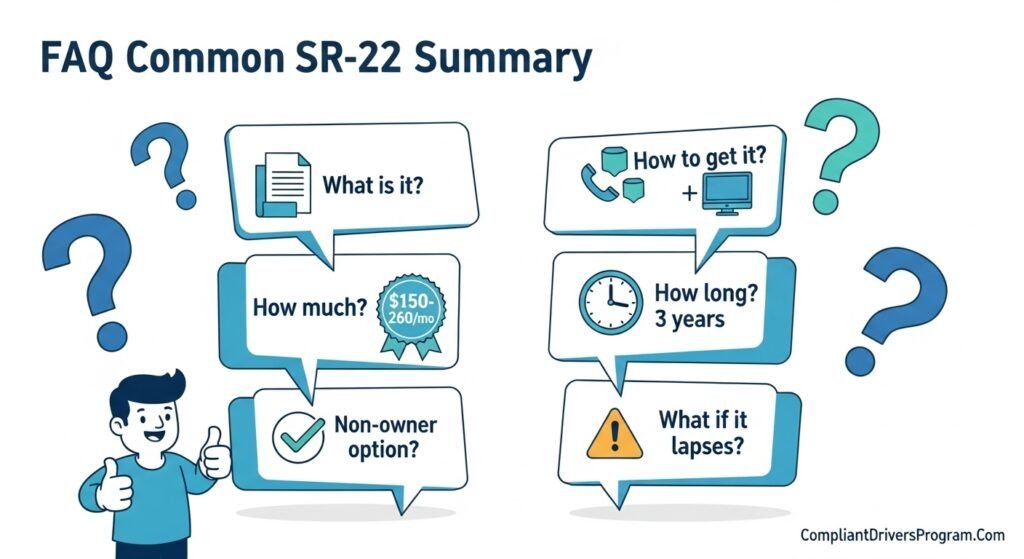

A: It’s a financial responsibility form your insurer files to prove you carry at least minimum liability coverage after a serious violation.

A: Call an insurer that offers SR-22, ask for SR22 filing, pay the filing fee, and keep coverage active without any gap.

A: Many drivers pay between $150 and $260 per month, depending on their state and violation, plus about a $25 filing fee.

A: It reports that you carry state minimum liability coverage; it doesn’t add collision or comprehensive protection by itself.

A: Yes. Non owner SR-22 policies are often cheaper because they only include liability on cars you don’t own.

A: Usually about 3 years, though some states require anywhere from 1 to 5 years based on the offense.

A: Your insurer must notify the state, and your license can be suspended again until you file a new SR-22 and restart compliance.

Final Thoughts and Next Steps

Here are the key points about SR-22 Insurance you should remember:

- It’s a financial responsibility form that proves you carry the required liability coverage.

- You usually need it after a DUI, suspension, or serious violation and must keep it for 3+ years.

- SR 22 insurance cost is higher, but you can still save money with smart shopping, safe driving, and simple cars.

- You can use non owners SR-22 if you don’t own a vehicle but still need to drive.

Your best next step is to get a few quotes from companies that specialize in high risk drivers and SR-22 filing, then compare them with options like Cheap Car Insurance and Second Chance Auto Insurance. The sooner you start, the sooner you’ll finish your SR-22 period and move toward normal rates again.

SR-22 Cost Calculator

Get Your Personalized 2026 SR-22 Insurance Estimate

Your Location & Profile

Violation Information

Final Details

Calculating Your Personalized Estimate…

Your SR-22 Estimate is Ready!

Based on 2026 rates for your state

Information about your state’s requirements.

Your Estimate Breakdown

Smart Tips to Lower Your Cost

This article is for information only. Please consult a licensed insurance professional or your state DMV before making coverage or legal decisions.

Leave a Reply