Here’s the thing: when you’ve had tickets, accidents, or a DUI, car insurance can feel brutal. You see a quote, your jaw drops, and you wonder if anyone will ever treat you fairly again.

If that sounds like you, you’re in the right place. This guide breaks down high risk auto insurance in clear, simple language, and shows you real steps to pay less in 2026.

You’ll learn what “high risk” really means, what non standard auto insurance is, how much it costs, how to find high risk driver insurance that actually helps you rebuild, and how to move back toward normal rates as fast as possible.

What Is High Risk Auto Insurance in 2026?

Most people don’t know this: insurance companies don’t “hate” you if you have a bad record. They just price your risk based on numbers and past claims.

High risk auto insurance is coverage built for people that standard companies see as more likely to file claims. These drivers are placed into a substandard insurance or non standard auto insurance tier.

You might need high risk driver insurance if you:

- Have multiple speeding tickets or serious violations

- Caused one or more at‑fault accidents

- Have a DUI or reckless driving charge

- Let your coverage lapse for weeks or months

- Have very poor credit or almost no insurance history

In simple terms, the company sees more risk, so you see higher premiums. But that label doesn’t have to last forever.

Why Being Labeled “High Risk” Really Matters

Here’s why this matters more than most drivers think. Once you’re tagged as “high risk,” several things usually happen at once:

- Fewer companies want to insure you

- The companies that accept you may charge 50% to 100% more

- You may be forced into assigned risk pools in some states

- You might need an SR‑22 filing after certain violations

If you ignore the problem and drive uninsured, you stack even more issues. You could face license suspension, fines, and more future rate hikes when you finally go back to an insurer.

If your license is already in trouble, take a look at Insurance for Suspended License for simple steps to get compliant again.

Who Gets Treated as a High Risk Driver?

Most people think only wild drivers with tons of DUIs are “high risk.” That’s not true. In 2026, many regular drivers fall into this group because of a mix of factors.

You may be seen as high risk if you have:

- A bad record with several speeding or red‑light tickets

- One or more at‑fault accidents in the last 3 years

- A DUI or other serious violation like reckless driving or hit‑and‑run

- Long gaps with no insurance

- Poor credit in states that allow insurers to use scores

- Very little driving history, like brand‑new or very young drivers

Commercial reports in 2024 and 2025 also show more violations and higher claim costs, which pushed many companies to tighten their rules and raise rates.

If that sounds like you, don’t panic. You just need to move into the right non standard auto insurance or substandard insurance lane for a while.

How High Risk Auto Insurance Works Behind the Scenes

Most people don’t know this part. When you apply, insurance companies pull several data sources at once:

- Your motor vehicle record (tickets, accidents, suspensions)

- Your claims history through databases like CLUE

- In many states, parts of your credit information

- Vehicle details, garaging zip code, and annual mileage

Then they rate you using their own formulas. If your risk is higher than their standard range, they may:

- Offer a policy but at a higher premium

- Push you into a non standard auto insurance program they own

- Decline to quote you at all

If many carriers decline, your state’s assigned risk plan may be the fallback. This is a last‑resort safety net so you can still meet legal requirements to drive.

Cost of High Risk Auto Insurance in 2026

You’re probably wondering about real numbers. Here’s what recent data and market trends show.

According to major rate studies, the average cost of high risk auto insurance is around $2,800 per year, or about $230 per month, compared to roughly $1,600 to $1,800 for a clean driver.

Bankrate’s 2026 analysis shows how one serious issue changes full‑coverage prices:

| Situation | Approx. Annual Premium | Change vs. Clean Record |

|---|---|---|

| Clean driver | $1,700 | — |

| Speeding ticket | Around $3,300 | Roughly +22% |

| At‑fault accident | Around $3,800 | Roughly +40% |

| DUI conviction | Around $5,300 | Roughly +95% |

| Teen high‑risk driver | Around $5,700 | Over +100% |

For drivers needing SR‑22 after a DUI, Forbes data shows yearly costs around $3,200–$3,500 in many states, plus a small filing fee of about $25.

If you only drive but don’t own a car, non‑owner SR‑22 policies can be much cheaper, often around $30–$85 per month in 2025. You can learn how regular non‑owner coverage works at Non Owner Car Insurance.

Non Standard Auto Insurance Market in 2024–2026

Here’s something most guides skip. The non standard auto insurance market went through a rough patch, then started recovering.

AM Best and other analysts report that nonstandard carriers were losing money badly in 2021 and 2022, but they turned things around in 2023 and 2024 after raising rates, tightening underwriting, and using better data tools.

A few key trends that affect your high risk auto insurance cost now:

- Nonstandard insurers improved from big underwriting losses to small gains

- Combined ratios (a measure of profit) dropped below 100 in 2024 and improved again in early 2025

- Direct premiums written in nonstandard auto grew by about 24% in the first half of 2024

- Overall U.S. auto rate increases slowed from about 15% in 2023 to around 10% in 2024

For you, this means something important. Rates are still higher than a few years ago, but big “emergency” hikes are easing, and some carriers are slowly competing harder again.

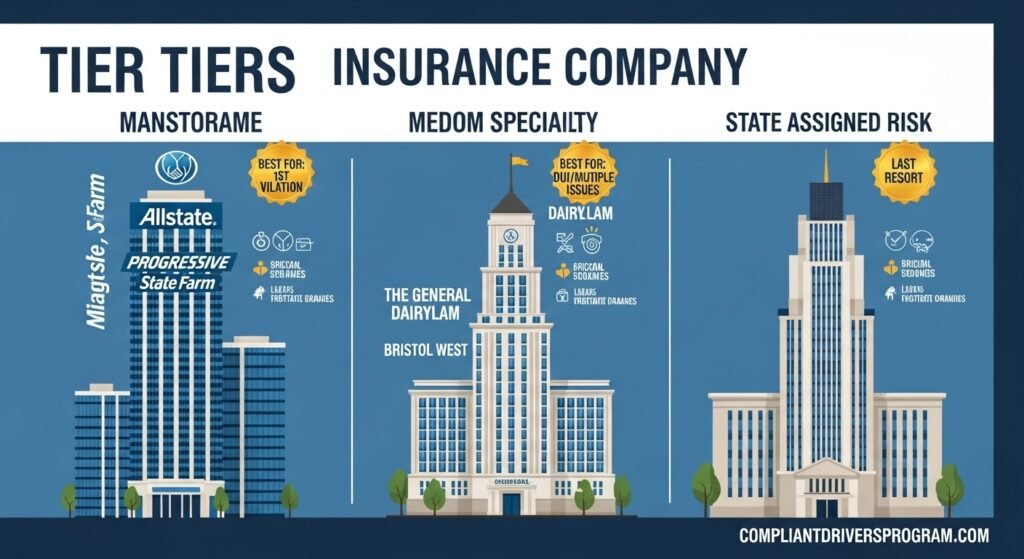

Best High Risk Insurance Companies and Options

Most people search “best high risk insurance companies” and hope there’s one magic name. In reality, the “best” company depends on your exact situation.

Different insurers focus on different types of high‑risk drivers:

| Company Type | Strength | Typical Role for High Risk Drivers | Best For |

|---|---|---|---|

| Mainstream national (like Allstate, Progressive, State Farm) | Strong discounts, apps, telematics | May keep you after a first violation and file SR‑22 | Drivers with 1 serious issue but otherwise ok |

| Specialty insurers (like The General, National General, Dairyland, Bristol West) | Very flexible underwriting | Focus on substandard insurance and tough cases | Drivers with DUIs, lapses, multiple tickets |

| State assigned risk plans | Guaranteed acceptance | Last resort option with limited choice | Drivers rejected by several companies |

Insurify’s late‑2025 data from one state shows The General, Dairyland, and Bristol West quoting in the low‑to‑mid $200s per month range for SR‑22 drivers, with other carriers higher or lower depending on location.

If you’re bouncing back after a DUI, read Insurance After DUI for step‑by‑step guidance that fits these kinds of companies.

Step‑by‑Step: How to Get High Risk Auto Insurance

Most people don’t know where to start once they get a cancellation or scary renewal notice. Here’s a clear path.

1. Pull your full driving record

Don’t guess. Order your record from your state DMV website or local office.

Look for:

- Dates of each violation and accident

- Any notations about DUI, reckless driving, or suspensions

- Any older items that should have dropped off

If you see mistakes, contact the DMV right away. Fixing even one incorrect accident or violation can lower your rate.

2. Decide what coverage you actually need

Here’s the thing: you don’t always need every bell and whistle when you’re rebuilding.

Think through:

- Liability limits (the minimum vs. higher limits for better protection)

- Whether you really need full coverage on an older car

- If dropping extras like rental or roadside makes sense for now

To understand minimum vs. higher limits better, check out Liability Insurance Car.

3. Shop smart and compare at least 5–7 quotes

Don’t stop at one quote. Many specialty insurers only shine for certain driver types.

Use online tools to get Car Insurance Quotes from several companies at once, and be honest about your accidents, violations, and DUI history. You can start with Car Insurance Quotes to make this easier.

Collect the offers, then compare:

- Total price

- Deductibles

- Fees for SR‑22 filings if needed

- Customer service reviews

4. Ask directly about SR‑22 or FR‑44

If your state requires an SR‑22 after a DUI or serious violation, you must file it on time. Some states use FR‑44 for higher limits.

National data from 2024 shows SR‑22 drivers often pay almost double what clean drivers pay, with an average near $3,300 per year after a DUI.

To understand the filing and cost differences by state, visit SR-22 Insurance Cost by State and SR-22 Insurance.

5. Lock in continuous coverage

Most people don’t know this: a coverage lapse of even 30 days can raise your rate by nearly 10% later.

So once you find a high risk auto insurance policy you can afford, keep it active:

- Pay on time or set up auto‑pay

- Avoid letting it cancel, even for a few days

- Contact the company early if you struggle with a payment

Comparison Table: High Risk Options in 2026

Here’s a simple table to compare the main paths you might face.

| Option | Cost Range (Annual) | Time Needed to Get Covered | Effectiveness | Best For |

|---|---|---|---|---|

| Standard insurer, 1 ticket | $1,800–$2,400 | 1–3 days | Medium | Mild bad record, first violation |

| Non standard auto insurance company | $2,400–$4,500 | Same day–3 days | High | Multiple accidents, DUI, or lapses |

| State assigned risk plan | $3,000–$5,500+ | 1–2 weeks | High for legal needs | Drivers rejected by several companies |

| Non‑owner SR‑22 policy | $360–$1,000+ | 1–3 days | High if you don’t own a car | Drivers who just need to satisfy SR‑22 requirements |

Numbers are typical ranges from 2024–2025 studies and will vary by state, age, vehicle, and record.

How Long Will You Be Considered High Risk?

Most people don’t realize that time is your biggest friend here. Your “high risk” label fades slowly as old problems age off your record.

Typical time frames in many states look like this:

| Issue | Time It Often Affects Rates | Notes |

|---|---|---|

| Minor ticket | Around 3 years | Impact drops a bit each year |

| At‑fault accident | Around 3–5 years | Bigger claims may hurt longer |

| DUI or reckless driving | Around 5–7 years | Some states keep it longer |

| Lapse in coverage | Around 6–36 months | Also depends on new driving behavior |

Here’s the key: the more clean time you stack, the better your offers become. Many people see real drops after 1–2 clean years and bigger drops after 3–5 years.

If you’ve struggled with tickets in the past, read Insurance for Bad Driving Record for strategies that fit long‑term rebuilding.

How to Lower High Risk Auto Insurance Rates (Fastest Wins)

Quick tip: you don’t need to wait five years to see savings. You can start trimming your high risk auto insurance cost over the next few months.

Here are moves that help in 2026:

- Take a defensive driving course

Many insurers still offer 5–10% off for an approved course, especially for drivers with violations. Check your state’s DMV site for a list of accepted classes. - Choose a safer, cheaper car to insure

Sports cars, big luxury SUVs, or heavily modified vehicles cost more to cover. Switching to a simple sedan or mid‑size SUV can help. - Raise your deductibles

Moving from a $500 to a $1,000 collision deductible can shave your monthly payment, but make sure you can afford that deductible if you crash. - Use usage‑based or telematics programs

Some companies offer discounts if you let them track your driving with a phone app or plug‑in. Safe driving data can help fight against your old bad record. - Grab every discount you legally can

Look into Safe Driver Discount, Accident Free Discount, good student, multi‑car, or bundle discounts where they apply. - Shop again every 6–12 months

As old accidents and violations age, your profile changes. Re‑quote your coverage regularly and use a tool like Cheap Car Insurance to keep track of better offers.

Pro Tip: Want a full list of savings steps you can actually do this week? Visit How to Lower Car Insurance Rates and pick two actions to start now.

Special Case: High Risk Drivers After a DUI

A DUI is one of the biggest triggers for high risk auto insurance. It usually brings:

- License suspension or restrictions

- SR‑22 or FR‑44 filing requirement

- Higher liability limits in some states

- Premiums that can nearly double

Forbes’ 2024 data shows the average annual cost for SR‑22 drivers with a DUI around $3,295, but some states go well above that.

If you’re in this situation:

- Ask your lawyer or court officer exactly how long you need SR‑22

- Start with Insurance After DUI for tailored guidance

- Compare both specialty insurers and major carriers willing to file SR‑22

- Keep your record clean from this point, since another violation can push you into the most expensive tiers

Special Case: Second Chance Coverage for Very Bad Records

Some drivers face more than one serious issue at once. Maybe you had a DUI, a previous accident, and a coverage lapse. That can feel hopeless.

Here’s the good news: some specialty insurers build products exactly for this situation. They often have flexible payment plans and allow more violations, as long as you’re willing to pay a higher rate for a while.

If this sounds like you, read Second Chance Auto Insurance to see how these companies work and how you can use them to rebuild.

Your job is simple: keep that policy active, avoid any new accidents or violations, and slowly move into better‑priced tiers over the next few years.

Choosing the Right Coverage Type as a High Risk Driver

Most people don’t think about the balance between cost and protection. When you’re high risk, that balance matters even more.

Here’s a quick guide:

- Liability‑only policy

Cheapest option and meets legal minimums. Works better for older cars that aren’t worth much. - Full coverage (liability + comprehensive + collision)

More protection, especially if your car is newer or financed. Costs more, but may be worth it if you can’t afford to replace the car. - Non‑owner policy

Great if you don’t own a car but need to keep insurance history or meet SR‑22 requirements.

To get a feel for what’s smart for your car’s value, use Liability Insurance Car as a starting point.

What to Avoid as a High Risk Driver

Here’s what can secretly keep you stuck in high risk auto insurance for longer than needed:

- New tickets

Even one fresh violation can reset your “clean time” clock. - Driving without insurance

Another lapse makes the next insurer nervous and adds to your rate. - Lying on applications

Companies will see your accidents and violations when they pull your reports. False answers can lead to cancellation or denied claims. - Over‑insuring beyond your budget

Don’t choose a policy so expensive you can’t keep it active. A slightly leaner policy you can maintain is better than rich coverage that cancels.

FAQ: High Risk Auto Insurance in 2026

A: Ask specialty insurers that sell non standard auto insurance, then check your state’s assigned risk plan if you’re still declined.

A: Major options include mainstream carriers willing to file SR‑22 and specialty insurers like The General, National General, Dairyland, and Bristol West, but the “best” choice depends on your state and record.

A: Many drivers pay between about $3,000 and $5,500 per year after a DUI, especially when SR‑22 is required, depending on state, age, and other violations.

A: Expect roughly 3–5 years for many accidents and violations, and up to 5–7 years for DUI or reckless driving, though this varies by state.

A: You can’t erase risk instantly, but you can make it cheaper by raising deductibles, taking courses, keeping coverage active, and using tools like Cheap Car Insurance to compare deals.

A: Yes. Both terms describe companies and policies built for drivers with a bad record, violations, accidents, or special filings like SR‑22.

Conclusion: Your Next Step Toward Better Rates

Here’s what you can do right now to move forward with high risk auto insurance in 2026:

- Know your record so there are no surprises.

- Use non standard auto insurance or substandard insurance as a stepping stone, not a life sentence.

- Keep coverage active while you stack clean time and avoid new violations or accidents.

- Hunt for discounts and re‑shop often, using tools like Car Insurance Quotes and Cheap Car Insurance.

Most people don’t realize how quickly things can improve once they get serious about safe driving and smart shopping. Start today, and your future renewals will look a lot better than they do right now.

High Risk Insurance Quote Tool

Estimate Your Rates • Assess Risk Level • Get Smart Savings Tips

| Violation | Duration | Rate Impact |

|---|---|---|

| Minor Ticket | ~3 years | +22% |

| At-Fault Accident | 3-5 years | +40% |

| DUI/DWI | 5-7 years | +95% |

| Coverage Lapse | 6-36 months | +10% |

| Type | Best For | Cost Level |

|---|---|---|

| Mainstream (Allstate, Progressive) | 1st violation, mild record | Lower |

| Specialty (The General, Dairyland) | DUI, multiple issues | Medium |

| State Assigned Risk | Rejected by others | Higher |

| Non-Owner Policy | No car, need SR-22 | Lowest |

| Driver Situation | Est. Annual | vs Clean |

|---|---|---|

| Clean Driver | $1,700 | Baseline |

| Speeding Ticket | ~$3,300 | +22% |

| At-Fault Accident | ~$3,800 | +40% |

| DUI Conviction | ~$5,300 | +95% |

| Teen High-Risk | ~$5,700 | +100% |

This article is for information only. Please consult a licensed insurance or financial professional before making decisions.

Leave a Reply