Here’s the thing: a DUI can feel like it wrecked your life overnight. Your license is at risk, your job might be affected, and then your insurance after DUI quote shows up and nearly doubles or more.

You might feel stuck and ashamed, but you’re not alone. Millions of drivers carry auto insurance after DUI or DUI car insurance every year and slowly rebuild their records. You can do the same with the right plan.

You’ll learn how insurance rates after DUI really work, how SR-22 required filings impact your costs, how long the rate increase can last, and step-by-step how to get insurance after DUI without overpaying. You’ll also see real numbers, 2025–2026 data, and tips most people never hear from an agent.

Understanding Insurance After DUI in 2026

What Is Insurance After DUI?

Most people don’t know this, but there’s no special “DUI policy” in the law. Insurance after DUI just means you’re now placed in a high‑risk group and priced like it.

Insurers may label it drunk driving insurance, insurance after DWI, or “high-risk coverage,” but it’s still a standard auto policy with higher premiums and sometimes extra filings like an SR-22 required form.

The big change is how insurers see you. You’re now flagged as someone more likely to cause a serious claim. That’s why insurance cost after DUI jumps so sharply, especially within the first renewal after your conviction.

Pro Tip: If your record already had accidents or tickets, your jump will be larger than someone who had a clean record before their first DUI.

DUI vs DWI: Does the Label Matter for Insurance?

Here’s the thing: some states use DUI (Driving Under the Influence), others use DWI (Driving While Intoxicated), and some use both.

For insurance companies, both mean the same thing—serious alcohol or drug‑related driving offense. Whether your state calls it DUI or DWI, you’ll still pay high‑risk prices for DUI car insurance or insurance after DWI.

The exact wording matters more in court than in your policy. For your insurer, it’s simply a major violation that stays on your record for several years.

How Much Does Insurance Go Up After DUI in 2026?

Current 2025–2026 Rate Increases

You’re probably asking: how much does insurance go up after DUI in 2026?

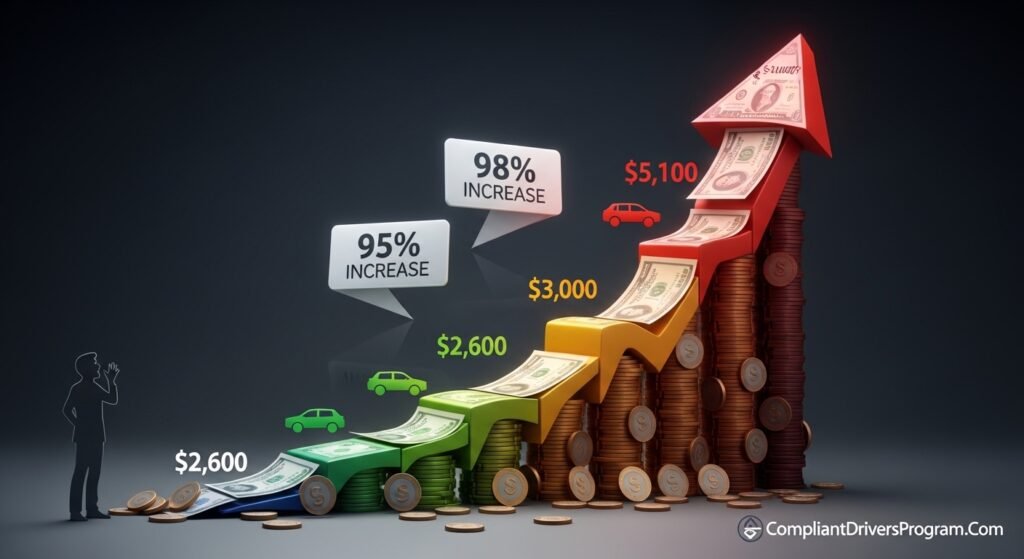

According to 2025 data from Insurance.com and Bankrate, a single DUI can push full‑coverage premiums from about $2,600 to over $5,100 per year in the U.S., nearly a 95% jump on average. Minimum coverage can climb from around $770 to $1,530, about a 98% increase.

Insurance.com also shows that at age 40, the average annual premium jumps from about $1,897 to $3,853, which is a 103% rate increase for a middle‑aged driver after one DUI.

Most people don’t realize this is often the single biggest cost of a DUI, even more than fines or court fees over the long run.

Company‑by‑Company Differences

Not all insurers react the same way to a DUI. Some raise premiums slightly, others double them or more. Insurance.com’s 2025 breakdown shows:

- GEICO average premium: about $1,338 before a DUI and $2,484 after, around an 86% increase.

- Progressive average premium: about $1,742 before, $2,266 after, roughly a 30% increase.

- State Farm average premium: about $1,713 before, $1,820 after, only around a 6% increase in some scenarios.

That means the “best insurance companies after DUI” for you may be very different from what worked before your conviction.

Pro Tip: Always compare new quotes right after your DUI. Your old company may no longer be your cheapest option, even if they keep you.

How Long Do High DUI Insurance Rates Last?

How Long After a DUI Does Your Insurance Go Down?

Most people ask, how long after a DUI does your insurance go down and return closer to normal.

Bankrate’s 2025 analysis shows that in many states, a DUI affects your insurance rates after DUI for three to five years, depending on local laws and your insurance company’s rating rules. Some carriers start lowering rates after three claim‑free years, while others wait until the full five‑year mark.

During that time, each clean year helps more than you think. A steady clean record, no new tickets, and no lapses can slowly shrink that rate increase over time.

SR‑22 Timeline and License Reinstatement

In many states, especially after a serious drunk driving offense, the SR-22 required period usually lasts about three years if the violation was a DUI or DWI, according to a 2025 SR‑22 guide.

During those years, you must:

- Keep continuous coverage with no gaps.

- Pay on time every month.

- Maintain at least your state’s minimum liability limits.

If your policy cancels, your insurer must notify the state, which can lead to another suspension and a restart of your license reinstatement timeline.

The Special Case: Insurance After DUI in Arizona

Arizona DUI and SR-22 Rules

If you’re in Arizona, things can feel even tougher. Arizona laws classify several levels of DUI, including “extreme” and “super extreme,” and many of these trigger SR-22 required filings plus license suspensions.

An Arizona DUI conviction adds 8 points to your driving record, which usually leads to a license suspension or revocation and a sharp premium increase. A Scottsdale DUI resource notes that a 40% or higher premium increase after DUI is common, and many drivers must file an SR‑22 to restore driving rights.

UNO Insurance Agency in Arizona confirms that SR‑22 filings are standard when a driver’s license is suspended due to DUI, driving without insurance, or other serious violations.

Pro Tip: If you’re in Arizona and need high‑risk coverage, look into High Risk Auto Insurance and SR-22 Insurance Cost by State to see how your costs compare to other states.

Average SR‑22 Costs in Arizona

In 2025, one SR‑22 cost analysis for Arizona shows that drivers with a first DUI/DWI offense face an average annual premium around $3,091, while a second DUI can push that to around $4,449 per year. A driver who simply needs SR-22 with 1 DUI might see a typical premium near $3,674 annually.

The filing fee itself is small—often $25–$50—but the heavy impact lies in your yearly premiums.

Step‑by‑Step: How to Get Insurance After DUI

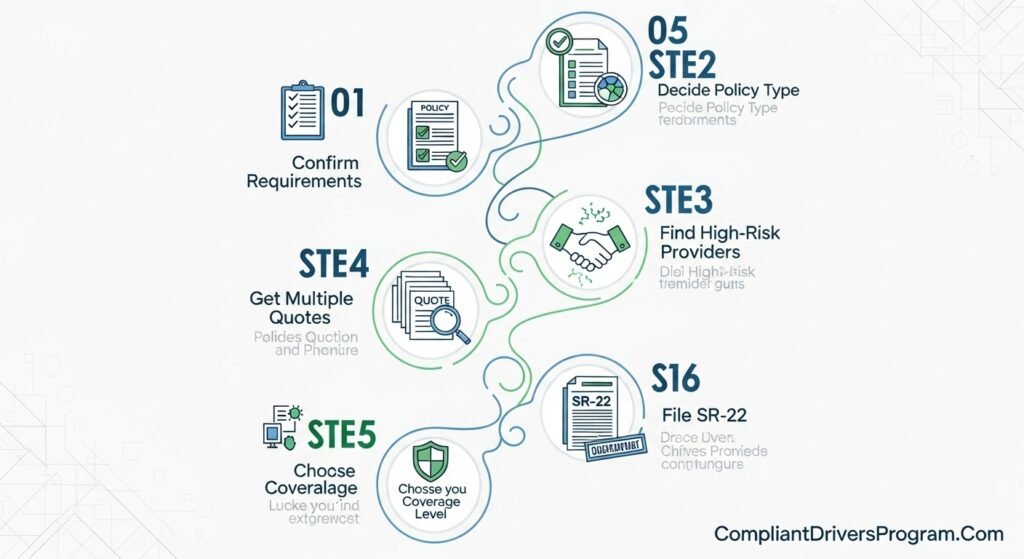

Step 1: Confirm Your License and Court Requirements

Before you shop for insurance after DUI, you need to know exactly what your state expects. Bankrate’s 2025 DUI cost guide stresses that each state sets its own rules for license suspension length, license reinstatement, and SR‑22 requirements.

Check:

- How long your license is suspended.

- Whether you must install an ignition interlock device.

- Whether SR-22 required applies and for how many years.

Your state DMV website or court paperwork should clearly explain this.

Step 2: Decide What Type of Policy You Need

Here’s the thing: not everyone needs the same type of coverage after a DUI. You might need:

- A normal auto policy if you own a vehicle.

- Non owner car insurance if you don’t own a car but need to drive occasionally, such as for work.

- A policy tailored to high‑risk drivers who already have multiple tickets or at‑fault accidents.

If your license was suspended and you’re trying to get it back, review Insurance for Suspended License to understand how coverage ties into reinstatement. That resource explains how insurers and DMVs coordinate after suspensions.

Step 3: Look for High‑Risk and “Second Chance” Providers

Most standard insurers prefer clean drivers. After a DUI, you may need companies that focus on high‑risk coverage or second chance auto insurance.

Dedicated providers and brokers who handle risky drivers can help you find insurance cost after DUI that fits your budget better than a big-name company that doesn’t want your risk level. Guides like Insurance for Bad Driving Record and Second Chance Auto Insurance can give you a starting point for these options.

These companies often:

- Offer SR-22 required filings directly.

- Accept more violations on your record.

- Help you step down to lower prices as your record improves.

Step 4: Get Multiple Quotes After DUI

You should never accept the first quote you see. 2025 rate studies show huge gaps between the cheapest and most expensive quotes after DUI offered to the same driver.

Use tools like Car Insurance Quotes to compare several insurers quickly. Make sure you enter your DUI honestly—hiding it won’t work since companies check your motor vehicle record anyway.

Look for:

- Total yearly cost, not just monthly.

- Whether they include SR-22 required filings.

- Any extra fees if you cancel early.

Step 5: Choose Coverage Level Carefully

Here’s the thing: full coverage is great, but after a DUI, it can be very expensive. Some drivers switch to liability‑only to keep costs manageable, especially if their car isn’t worth much.

To see what liability covers, review Liability Insurance Car. It explains how liability pays for other people’s injuries and property damage, which is usually what states require as a minimum.

If you still owe money on your vehicle, your lender might require collision and comprehensive coverage. That’s why you can’t always drop to minimums right away.

Step 6: File Your SR‑22 (If Needed)

By early 2026, SR‑22 rules haven’t changed much. Allstate’s 2026 update explains that SR-22 isn’t a type of insurance, but a form your insurer files with the state, proving that you meet minimum liability limits.

You usually need SR‑22 if you:

- Have a DUI or DWI conviction.

- Had your license suspended or revoked.

- Were caught driving without insurance.

According to one 2025 SR‑22 insurance guide, the filing period often runs from 1 to 5 years, with 3 years standard for DUI convictions in many states.

Remember:

- The filing fee is small.

- The major cost is the insurance cost after DUI and the high‑risk rating attached to your policy.

If you’re comparing states, SR-22 Insurance Cost by State gives a helpful overview of how different violations affect rates.

Cost and Time Expectations After a DUI

Typical Cost Ranges in 2026

Using 2025–2026 data from Insurance.com and Bankrate, here’s what many drivers face for auto insurance after DUI:

- Average full‑coverage premium before DUI: around $2,600–$2,700 per year.

- Average after DUI: around $5,100+ per year for full coverage.

- Minimum coverage before: about $770 per year.

- Minimum coverage after: around $1,530 per year.

In high‑cost states, numbers can be much higher. In cheaper states, they may be lower, but the rate increase percentage is still steep.

If you live in a state like Arizona, SR‑22 premiums after a DUI often land in the $3,000–$4,500 per year range for at least the first offense.

How Long Until You See Relief?

Most people don’t know this, but you can start seeing small drops within 2–3 years of clean driving, even if a DUI remains on your record.

However, big changes usually come at major milestones:

- At 3 years: many insurers treat you as less risky if you’ve had no new violations or claims.

- At 5 years: in some states, your DUI influence on premiums shrinks further, especially if it’s your only major offense.

Pro Tip: Mark your calendar every renewal period. Shop again every 6–12 months using sites like Cheap Car Insurance to see if another company will now treat you more kindly.

Comparison Table: DUI Insurance Options

Here’s a simple comparison of common post‑DUI insurance paths:

| Option | Cost (Per Year) | Time Needed | Effectiveness | Best For |

|---|---|---|---|---|

| High‑risk full coverage policy | $3,500–$6,000+ | 3–5 years | High protection, high cost | Newer car, active loan |

| Liability‑only DUI car insurance | $1,500–$3,000 | 3–5 years | Medium protection | Older paid‑off cars |

| Non owner car insurance SR‑22 | $600–$1,500 | 1–3 years | Low–medium protection | No car, need license reinstatement |

| Second chance auto insurance program | $1,800–$3,500 | 2–4 years | Medium–high savings over time | Drivers rebuilding bad records |

Costs are approximate national ranges based on 2025–2026 high‑risk pricing trends.

Powerful Ways to Lower DUI Insurance in 2026

Use Discounts Most Drivers Forget

You might think you’re locked into sky‑high rates forever, but there are still ways to save. Some carriers still offer:

- Safe driver discount after a set number of clean years post‑DUI.

- Accident free discount if you avoid new at‑fault crashes.

- Multi‑policy discounts if you bundle home or renters coverage.

You can explore how these work through Safe Driver Discount and Accident Free Discount. Once enough time passes after your conviction, these discounts help offset the rate increase.

Adjust Your Policy Smartly

Most people don’t know this, but you can dial‑in your coverage to balance risk and price instead of just dropping everything. Check How to Lower Car Insurance Rates for more detailed tactics.

Common moves include:

- Raising deductibles on collision and comprehensive.

- Removing extras like rental car reimbursement.

- Switching to a usage‑based program that tracks driving behavior.

Usage‑based telematics can be especially helpful after a DUI. If you prove you drive safely, some insurers give meaningful discounts even with high‑risk status.

Drive Less and Drive Safer

Safer driving is not just about avoiding another DUI. It also means:

- No speeding tickets.

- No phone use while driving.

- Avoiding late‑night driving where impairment risks are higher.

Safer habits reduce your chances of another violation, which keeps your insurance rates after DUI from climbing even more and helps them drop sooner.

If you don’t need to drive daily, consider carpooling, using rideshare apps, or public transit to lower your annual mileage. Many insurers offer lower rates if you drive less than 7,500–10,000 miles per year.

What to Avoid After a DUI Conviction

Most people focus on getting back on the road fast and forget how easy it is to make things worse. Avoid these mistakes:

- Forgetting to renew your SR‑22 and letting your policy lapse. This can restart your license reinstatement clock and trigger new suspensions.

- Ignoring court‑ordered programs like alcohol education or treatment. Non‑completion can lead to extended penalties and more SR‑22 time.

- Switching companies without confirming who will file your new SR‑22 right away.

If you’re not sure, talk to your agent before changing anything. It’s easier to ask questions upfront than to fix a brand‑new suspension later.

FAQ: Insurance After DUI in 2026

A: Confirm your state and court requirements, then shop multiple high‑risk insurers who handle SR-22 required filings, compare quotes, and choose coverage that fits your budget.

A: Many drivers see improvements after 3–5 years of clean driving, though some insurers begin minor reductions after 2–3 years without new violations.

A: 2025 data shows full‑coverage premiums often nearly double, from around $2,670 to over $5,185 per year, and minimum coverage nearly doubles as well.

A: Yes. Many insurers offer non owner car insurance with SR‑22 filings, which is useful if you don’t own a car but need your license reinstated.

A: It’s the same type of policy, but rated for higher risk. Premiums are higher, and in many states, there’s an SR-22 required filing tied to your policy.

Final Thoughts and Next Steps

Here’s what you should remember going forward:

- A DUI or DWI hurts, but you can still get insurance after DUI and drive legally again.

- Your insurance rates after DUI may nearly double at first, but each clean year helps lower them.

- Many states, including Arizona, tie license reinstatement to SR-22 required filings that usually last around three years for DUI convictions.

- High‑risk and second chance programs, plus smart shopping with tools like Cheap Car Insurance and Car Insurance Quotes, can save you hundreds or even thousands each year.

Your best next step is simple: gather your court and DMV papers, compare several 2026 DUI car insurance quotes, and choose a plan that keeps you legal while you rebuild your driving record.

🚗 DUI Insurance Cost Calculator

Estimate your insurance rates after DUI conviction

2025-2026 Data📈 Your Estimated DUI Insurance Costs

This article is for information only. Please consult a licensed insurance agent, attorney, or financial professional before making decisions about your coverage or legal situation.

Leave a Reply