Let’s be real. When your record has tickets, speeding, or at fault accidents, car insurance can feel impossible. You see huge price jumps, more points on license, and letters about rate increase that make your stomach drop.

You’re not a bad person. You just have a bad driving history right now. And yes, you can still get affordable auto insurance if you know where to look and what steps to take.

Here, we break down how insurance bad driving record really works, what companies look for, how much more you might pay, and real steps to lower your costs over time. You’ll also see the best insurance for bad driving record, ideas for cheap insurance with accidents, and how to slowly rebuild your record so rates drop again.

By the end, you’ll know exactly how to get insurance with accidents, handle multiple violations insurance, and stop feeling lost every time you get a quote.

This article is for information only. Please consult a professional before making decisions.

What “Insurance Bad Driving Record” Really Means

Here’s the thing. A “poor driving record insurance” situation doesn’t come from one little mistake. Insurers look at patterns in your driving.

Usually, you’re seen as high risk when you have several tickets, one or more at fault accidents, a DUI, or a lot of points on license. Each issue on its own can cause a rate increase, but together they push you into high risk auto insurance territory.

Most people don’t know this, but insurers often check three to five years of your history. Serious problems like DUI or reckless driving can sometimes affect you even longer, depending on state laws and company rules.

Quick tip: If you’ve had a clean year or two after some trouble, ask for new quotes again. Companies price insurance bad driving record based on how recent your issues are.

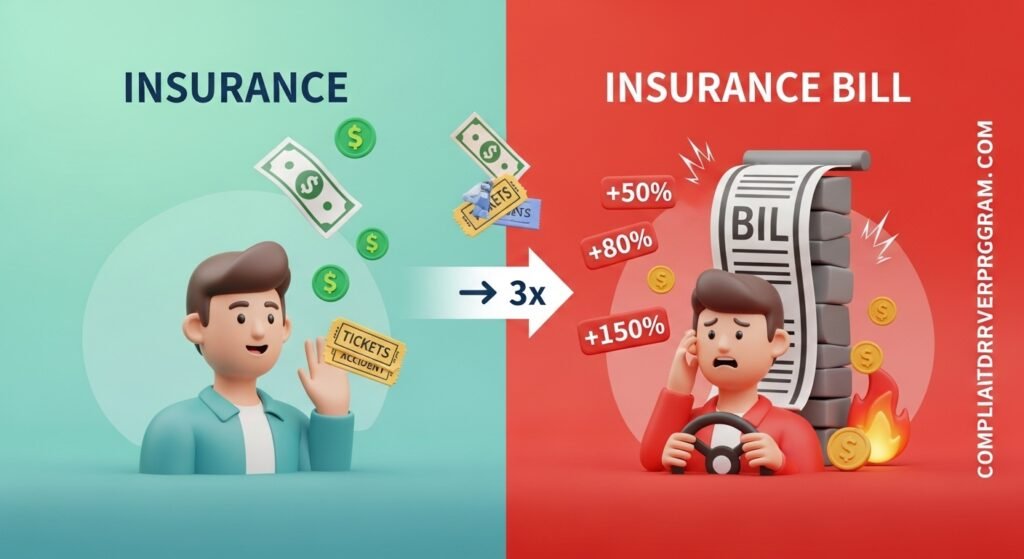

Why Your Rates Explode After Tickets And Accidents

Most people don’t know this, but not all violations are equal. Some things barely move your price, while others send your insurance with accidents bill through the roof.

- Minor tickets like 5–10 mph over the limit might bump your rate, but not as much as major speeding.

- Major speeding, reckless driving, and multiple tickets can almost double your poor driving record insurance costs.

- One at fault accident can raise your premium 30–50% or more, and more accidents can make some companies drop you.

According to Consumer Reports (2025), drivers with serious violations often pay hundreds more per year than similar drivers with clean records.

Most people don’t know this: if you get a DUI, you may need special SR-22 insurance filings just to stay legal, and average full coverage costs for drivers with DUI can jump well above 2,000 dollars per year in many states (Car and Driver, 2024).

Pro Tip: When you get a new ticket, don’t wait. Ask your agent if taking a defensive driving course can soften the rate increase before renewal.

Main Types Of Insurance Bad Driving Record Policies

Here’s the thing. You don’t just have one option when your record looks bad. Different policy types can help you stay on the road.

1. High risk auto insurance policies

If your record has multiple violations, at fault accidents, or DUI, many standard companies may say no. Instead, you may need high risk auto insurance through non‑standard carriers that focus on poor driving record insurance.

These plans cost more, but they’re designed exactly for insurance bad driving record problems. They’ll work with drivers who have tickets, suspensions, or lapses in coverage.

To learn more about this type of coverage, you can read about High Risk Auto Insurance.

2. Second chance auto insurance programs

Most people don’t know this, but some companies offer “second chance” style policies. These are made for people trying to rebuild after a rough few years.

You still pay more than a perfect driver, but you may get clear rules: drive claim‑free for 12–36 months, keep no new tickets, and your rate increase can start to reverse.

You can explore these options in more detail at Second Chance Auto Insurance.

3. State‑assigned risk pools

When no one says yes, you may still get coverage through a state‑assigned risk plan. These are last‑resort programs where insurers must accept high‑risk drivers who can’t find a policy elsewhere.

They usually cost more and may offer only basic coverage, but they help you stay legal and keep working on your record. Consumer groups like Consumer Reports note that these plans can be life savers when private companies all decline you.

4. Non owner car insurance for drivers without a car

Here’s something many drivers miss. If you don’t own a car but still need proof of coverage, you can get Non Owner Car Insurance.

This can be helpful if your license is suspended and you must file SR-22 insurance to get it back, or if you borrow or rent cars often.

You can learn more about this option at Non Owner Car Insurance.

Step‑By‑Step: How To Get Car Insurance With Bad Driving Record

If you want to know how to get insurance with bad record, follow these steps one by one.

Step 1: Gather all your driving details

Here’s the thing. You can’t hide your history. So it’s better to know exactly what’s on it.

- Count your tickets, speeding violations, and at fault accidents from the last three to five years.

- Check how many points on license you have and when they drop off.

- Look at any DUI, suspensions, or lapses in coverage you’ve had.

Many DMVs let you pull your driving record online for a small fee. Your report helps you understand how serious your insurance bad driving record situation is.

Step 2: Decide what coverage you really need

Most people don’t know this, but over‑insuring a car can cost you more than the vehicle is worth when you’re high risk.

Ask yourself: Is your car older and paid off? If yes, you might choose state‑minimum liability insurance car plus maybe uninsured motorist. Newer cars or financed cars may still need full coverage even with poor driving record insurance.

To understand liability limits better, read about Liability Insurance Car.

Step 3: Get several car insurance quotes at once

Quick tip: Never check just one company when you have insurance bad driving record trouble. Prices can be wildly different.

Use online tools or agents to compare Car Insurance Quotes from standard and high‑risk carriers. Some companies are way more friendly to insurance with accidents, while others focus on drivers with tickets but no crashes.

You can start with Car Insurance Quotes to see how different your options are.

Step 4: Look for SR-22 insurance if you need it

If you had a DUI, serious multiple violations, or a suspension, your state may require SR-22 insurance. This is a filing that proves you carry at least the minimum coverage.

You don’t buy SR‑22 by itself. You buy a policy and the company files the form for a fee. You can dig into details at SR-22 Insurance.

Curious about cost? There is also a helpful breakdown at SR-22 Insurance Cost by State that explains why some states are far more expensive than others.

Step 5: Check for insurance after DUI help

Here’s the thing. A DUI can feel like the end of affordable coverage, but there are specific insurance after DUI products.

Some insurers and brokers focus on drivers in this situation and help you meet court and DMV rules. You can learn more at Insurance After DUI.

Step 6: Fix any license issues fast

If your license is suspended, many states still let you carry insurance for suspended license so you can start the path back.

These policies often connect with SR‑22 filings and may be required before the DMV restores your full driving rights. You can study this more at Insurance for Suspended License.

Best Insurance With Accidents And Multiple Violations Insurance Options

Most people don’t know this, but the “best” company for insurance bad driving record changes based on your exact problem. Here’s how to think about it.

- One at fault accident, no DUI: Some major insurers may still cover you, just at a higher price.

- Several at fault accidents or multiple violations: You likely need high risk auto insurance or second chance auto insurance products.

- DUI plus tickets: You may need insurance after DUI with SR-22 insurance and higher limits.

According to a 2026 ranking by CNBC Select, big names like State Farm, Geico, Progressive, Erie, and USAA often offer lower‑than‑average prices for high‑risk drivers, though exact rates depend on your state and record.

Pro Tip: When you talk to agents, ask directly: “Do you have a plan for bad driving record drivers or second chance auto insurance?” This question quickly shows if they can actually help.

Cost And Time Expectations For Poor Driving Record Insurance

Here’s the thing. You won’t fix insurance bad driving record costs overnight, but you can plan your timeline.

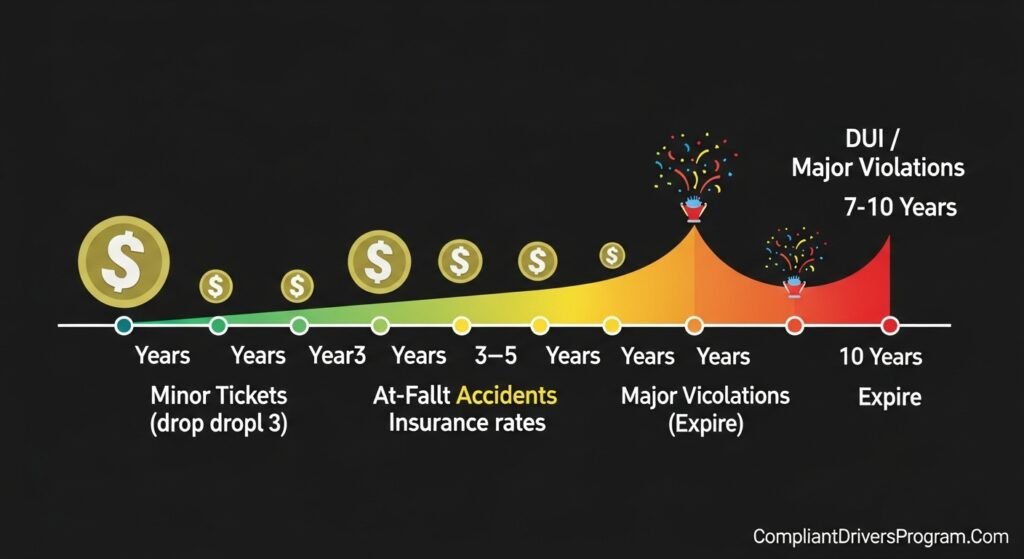

- After one at fault accident, higher rates often last three years, sometimes five.

- Minor tickets may affect you for three years, depending on state rules.

- DUI or major reckless driving can affect rates for up to ten years in some states.

Data from Car and Driver shows that full-coverage premiums for drivers with DUI or DWI can reach around 2,300 dollars per year on average, which is hundreds more than for clean drivers.

If you stay claim‑free and avoid new tickets, many insurers will slowly reduce your premium at each renewal once old issues age off your record. Consumer advocates recommend re‑shopping your policy every year while your record improves to catch these drops faster.

How To Make Cheap Insurance With Accidents More Likely

Most people don’t know this, but you can soften the pain even when your insurance with accidents rate is high.

1. Adjust your coverage level

You don’t want to be under‑insured, but you also don’t want to overpay when money is tight.

For older, low‑value cars, dropping collision or comprehensive and keeping strong liability insurance car can free up cash. For newer cars, you might raise deductibles instead of dropping coverage.

You can read more tips on this at How to Lower Car Insurance Rates.

2. Ask for every discount you can

Here’s the thing. Even with insurance bad driving record issues, you can still get some discounts.

Ask about:

- Multi‑car or multi‑policy bundles

- Good student discounts for younger drivers

- Auto‑pay or pay‑in‑full savings

- Vehicle safety device discounts

Some companies also start giving back Safe Driver Discount style savings after you go a set time with no tickets or accidents, even if your past is messy. You can explore that at Safe Driver Discount and Accident Free Discount.

3. Change how you use your car

Quick tip: Fewer miles often mean lower risk in the eyes of insurers.

If possible, drive less by carpooling, taking public transit, or working from home some days. Ask your insurer if they have a low‑mileage or telematics program that tracks your driving for a possible discount.

Habits That Slowly Turn A Bad Record Into A Better One

Most people don’t know this, but the best cheap insurance with accidents strategy is actually future‑focused. The goal is to make sure you stop adding new problems.

Build safer daily driving habits

- Leave 5–10 minutes earlier so you don’t feel rushed and tempted to speed.

- Use cruise control in known speed trap areas to avoid more speeding tickets.

- Put your phone in “do not disturb” and keep it out of sight.

Over time, clean driving reduces points on license, removes old violations, and builds a new story for your insurance bad driving record profile.

Take a defensive driving course

Many states and insurers let you remove points or get a small discount after passing an approved course.

According to State Farm, some insurers suggest taking a defensive driving class and checking online quotes often to better manage high‑risk costs.

Pro Tip: Ask your insurer which exact course they accept before you pay for anything. That way you’re sure it will actually help your poor driving record insurance cost.

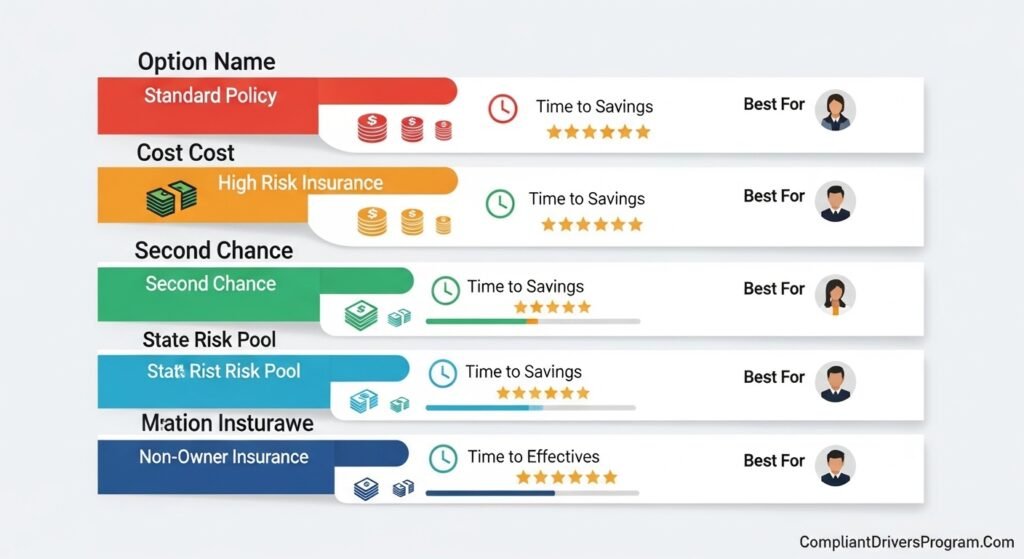

Quick Comparison Of Insurance Bad Driving Record Options

Here’s a simple table to show how different options usually look. Costs are rough ranges and will vary by state, company, and record.

| Option | Cost (per year) | Time Needed To See Savings | Effectiveness | Best For |

|---|---|---|---|---|

| Standard policy with higher rates | 1,800–3,000 dollars | 3–5 years of clean driving | Medium | Drivers with 1–2 tickets or one mild at fault accident |

| High risk auto insurance | 2,500–4,500 dollars | 3+ years, plus no new violations | High | Drivers with multiple violations insurance needs or serious issues |

| Second chance auto insurance | 2,000–3,500 dollars | 1–3 years of clean record | High | Drivers ready to improve habits after a rough patch |

| State‑assigned risk pool | 3,000–5,000 dollars | 3–5 years, then move to regular market | Low–Medium | Drivers rejected by several companies |

| Non owner car insurance with SR‑22 | 500–1,200 dollars | 2–3 years while rebuilding record | Medium | Drivers without a car who must keep coverage or meet court rules |

These ranges reflect typical differences between clean and high‑risk drivers mentioned by consumer insurance guides and industry data between 2023 and 2025.

FAQs About Insurance Bad Driving Record

A: The best insurance for bad driving record is usually a high risk auto insurance or second chance auto insurance policy that accepts your history and lets you lower costs as you drive safely over time.

A: To get cheap insurance with accidents, shop several quotes, adjust coverage, increase deductibles, ask for discounts, and focus on clean driving so older at fault accidents fall off your record.

A: To get car insurance with bad driving record fast, gather your driving record, check if you need SR-22 insurance, contact high risk auto insurance companies, and compare at least three Car Insurance Quotes the same day.

A: No. Insurance after DUI is expensive at first, but if you avoid new tickets or at fault accidents, many insurers lower rates after three to ten years, depending on your state.

A: Yes. You can often buy insurance for suspended license plus SR-22 insurance to start the reinstatement process, though you may only be allowed limited or no driving until the state clears you.

A: Most insurance bad driving record issues last three to five years, but serious violations like DUI can affect poor driving record insurance pricing longer in some states.

A: Non owner car insurance can be worth it if you don’t own a car but need continuous coverage, need SR‑22 filings, or want to prevent a lapse while you work on your record.

Conclusion: Turning Insurance Bad Driving Record Into A Comeback Story

Here’s the thing. A bad record feels heavy, but it doesn’t have to follow you forever. You can still find insurance bad driving record options that keep you legal while you rebuild.

Key ideas to remember:

- You have several choices, including high risk auto insurance, second chance auto insurance, and Non Owner Car Insurance.

- You can lower costs by changing coverage, asking for discounts, and improving habits to earn Safe Driver Discount and Accident Free Discount later.

- Time and clean driving are your strongest tools for turning poor driving record insurance into something more manageable.

Your next step? Gather your driving record, decide what coverage you truly need, then get several Car Insurance Quotes today. The sooner you start, the sooner your insurance with accidents story becomes a recovery instead of a burden.

This article is for information only. Please consult a professional before making decisions.

🚗 Driving Record Impact Calculator

Calculate how your driving history affects insurance rates & get personalized recommendations

Leave a Reply