Here’s the thing: a car crash can wreck more than just your car.

You might face hospital bills, therapy costs, and weeks of missed work. Your health insurance might not cover everything, and waiting for the at‑fault driver’s insurance can take months. That’s where personal injury protection steps in and helps you stay afloat.

You’ll learn what PIP insurance is, what PIP coverage pays for, how it works in states like personal injury protection Florida, personal injury protection Michigan, NY, Texas, and NJ, and how it compares to other coverages. You’ll also see when you might need a lawyer or attorney and how to decide if PIP makes sense for you.

By the end, you’ll know how to protect yourself, your family, and your wallet with smart injury coverage choices.

What Is Personal Injury Protection (PIP)?

Most people don’t know this, but personal injury protection is actually “no fault” medical coverage.

PIP coverage pays for your medical expenses and sometimes your lost wages, no matter who caused the crash. It follows you and your family, not just your car, and can apply when you’re a driver, passenger, or even a pedestrian hit by a vehicle.

In many no fault insurance states, you must carry PIP insurance by law. In other states, it’s optional but still very helpful because it pays faster than waiting for a liability claim.

Think of it like a quick cash shield that helps you handle bills right after a crash while the bigger claim gets sorted out.

How PIP Coverage Works After A Crash

Here’s the thing: PIP kicks in right after the accident, not months later.

After a covered crash, you file a PIP insurance claim with your own insurer. You send medical bills, proof of missed work, and any other cost records. Your insurer reviews them and pays up to your PIP coverage limit, such as 5,000, 10,000, or even 50,000 dollars.

The money can go directly to doctors or to you, depending on the bill. You don’t have to prove the other driver was at fault first, which speeds things up and lowers stress.

Most people use PIP alongside health insurance, so both help cover medical expenses from the same crash.

Pro Tip: Always report a crash to your insurer within 24–48 hours so your PIP insurance claim doesn’t get delayed.

What PIP Insurance Usually Covers

Most people think PIP only pays hospital bills, but it can do more.

Typical PIP coverage includes emergency room care, surgery, follow‑up visits, and physical therapy. It can also cover X‑rays, prescription drugs, and sometimes medical devices like crutches or braces. Many policies include part of your lost wages if you can’t work while you heal.

Some PIP insurance also pays for passenger coverage medical bills, funeral costs, and replacement services like hiring someone to clean your home or drive your kids. Coverage details depend on your state and insurer, so you always want to read your declarations page.

If you live in a no fault state, these benefits often replace your right to sue for small injuries, but not always for serious ones.

Why Personal Injury Protection Matters So Much

Most people don’t know this: medical bills are a top cause of debt in the U.S.

Personal injury protection helps you avoid draining your savings after even a minor crash. It pays faster than at‑fault claims and can fill gaps left by health insurance, like deductibles and co‑pays. This can matter a lot if your health plan has a high deductible of 2,000 dollars or more.

PIP insurance also helps self‑employed people and hourly workers who can’t afford time off. Because PIP often covers lost wages, it keeps money coming in while you recover.

For families with kids or older relatives who ride with you, PIP coverage also adds peace of mind, since passenger coverage is usually included.

Pro Tip: If your health insurance is weak or you have no disability coverage, bumping up PIP coverage limits can be one of your best money moves.

Personal Injury Protection Florida: Special Rules You Must Know

Here’s the thing about personal injury protection Florida rules: they’re strict.

The Florida personal injury protection statute requires most drivers to carry at least 10,000 dollars in PIP (Florida Department of Highway Safety, 2024). You must file for medical care under Florida personal injury protection insurance within 14 days of the crash, or you may lose benefits.

In Florida, no fault insurance means your own PIP insurance pays first for medical expenses, up to the limit. Serious injuries might still allow lawsuits against the at‑fault driver if you meet certain injury thresholds.

Because Florida has high crash and medical costs, many attorney ads focus on PIP disputes, billing issues, and claims denials.

Personal Injury Protection Michigan: Big Limits, Big Choices

Most people don’t realize how unique personal injury protection Michigan rules are.

Michigan used to require unlimited lifetime PIP coverage, making it one of the most generous but costly systems. Since reforms in 2020, drivers can now pick lower PIP limits like 500,000 or 250,000 dollars, or sometimes even less, to cut costs (Michigan.gov, 2024).

Unlimited PIP insurance in Michigan can cover long‑term care, rehab, and injury coverage that lasts for years, not just months. That’s huge if you face a serious brain or spine injury.

Because choices are complex, many people talk with an attorney or insurance agent before changing their personal injury protection limits.

Personal Injury Protection In New York And New Jersey

Quick tip: if you drive in NY or NJ, you deal with strict no fault state rules.

In New York, standard PIP coverage is often 50,000 dollars per person, and it pays for medical expenses, a portion of lost wages, and some other costs. Basic personal injury protection new york policies limit lawsuits for minor injuries, but you can sometimes sue for “serious injury” such as major fractures.

In NJ, personal injury protection nj offers several medical coverage options, sometimes up to 250,000 dollars, but the default may be lower. Drivers can choose “limitation on lawsuit” or “no limitation,” which affects your right to sue.

If you’re unsure which option to pick, a local lawyer who understands no‑fault rules can explain the trade‑offs in plain language.

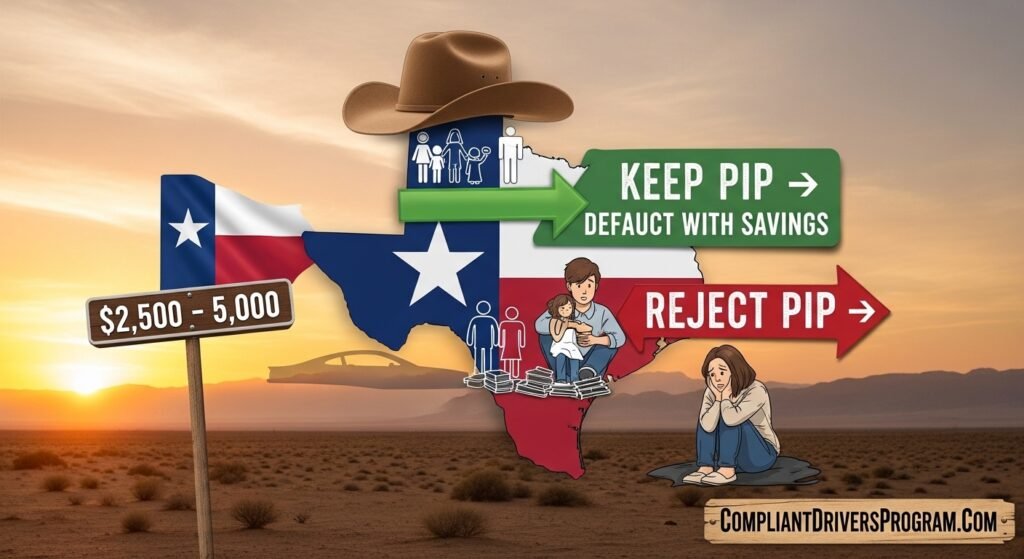

Personal Injury Protection In Texas: Is It Required?

Many people ask: is personal injury protection required in Texas?

In Texas, insurers must offer PIP insurance, but you don’t have to buy it. You can reject it in writing if you want to save money. If you don’t reject it, you’ll usually get at least 2,500 to 5,000 dollars of protection coverage Texas by default (Texas Department of Insurance, 2024).

Texas personal injury protection works much like other states: it pays medical expenses, lost wages, and some household services regardless of fault. It sits on top of your liability insurance car coverage, which protects others when you cause a crash.

For many Texas drivers with high deductibles, keeping at least some PIP coverage makes more sense than cutting it to save a few dollars.

Pro Tip: In Texas, ask your agent to show you quotes with and without PIP insurance so you see the real price difference before rejecting it.

Personal Injury Protection In Non‑Fault And Optional States

Here’s the thing: not every state is a no fault state.

Some states make personal injury protection optional instead of mandatory. In these places, you may rely more on medical payments (MedPay), health insurance, and the at‑fault driver’s liability insurance car. Optional PIP gives you extra injury coverage that kicks in quickly without proving fault.

If you often drive in ny, new york, florida, texas, nj, or nearby states, check whether your PIP coverage applies when you cross state lines. Many policies follow you across the U.S., but rules about lawsuits and limits still depend on where the crash happens.

A local attorney in that state can explain how PIP interacts with local no fault insurance rules if your case gets complex.

Personal Injury Protection vs Bodily Injury Liability

Most people confuse personal injury protection vs bodily injury coverage, but they’re very different.

Personal injury protection covers you and your passengers, regardless of fault. It helps with medical expenses, lost wages, and related costs right after a crash. You file a PIP insurance claim with your own company.

Bodily injury liability is part of your liability insurance car. It pays for injuries you cause to other people in a crash, such as another driver or pedestrian. They file against you or your insurer, not the other way around.

You want both: PIP to protect you and your family, and bodily injury liability to protect your assets if you hurt someone else.

Cost Of PIP Insurance And What Affects It

Quick tip: PIP insurance cost is usually lower than full collision and comprehensive.

Your PIP insurance price depends on your state, driving record, chosen limit, and sometimes your health coverage. Higher PIP coverage limits cost more but give better protection, especially in expensive medical states like personal injury protection florida or personal injury protection michigan.

In many states, adding 5,000–10,000 dollars of personal injury protection might add only 5–20 dollars per month to your premium. Choosing a deductible on PIP, when allowed, can cut the PIP insurance cost, but you’ll pay more out of pocket after a crash.

You can compare quotes using tools on insurer sites or work through guides like Average Car Insurance Cost and Cheap Car Insurance to see how PIP fits in your budget.

How To Apply For Personal Injury Protection (PIP Application)

Most people don’t know this, but your application for PIP often happens automatically when you buy auto insurance.

When you first sign up, your agent or online form shows PIP coverage options and limits. You choose the level you want, such as 5,000 or 25,000 dollars, and sign your application. In some places, you must sign a special form if you reject PIP or pick lower limits.

After a crash, the PIP application is really your claim form. You fill out accident details, list your injuries, and sign medical release forms so the insurer can review records.

Respond quickly to any follow‑up questions, or your PIP insurance payment might pause until they get what they need.

Step‑By‑Step: Using PIP Coverage After A Crash

Here’s the thing: a simple process can help you get paid faster.

- Report the accident

Call your insurer within a day or two and say you want to use personal injury protection. Ask what forms they need. - Get medical care right away

See a doctor as soon as possible, even if you “feel okay.” Many no fault state rules like Florida’s 14‑day rule require fast treatment to unlock PIP coverage. - Track every cost

Keep all bills, receipts, and proof of lost wages, such as notes from your employer. These documents support your PIP insurance claim. - Submit your PIP claim

Fill out the application or claim form, attach copies of your records, and send them in. Ask how long payments usually take and who to contact for updates.

Pro Tip: If bills start stacking up or an adjuster denies care, call an experienced lawyer or attorney who handles PIP disputes in your state.

How PIP Coverage Fits With Other Car Insurance Types

Most people don’t see how PIP coverage connects with other car insurance pieces.

You likely also carry property coverages like Collision Insurance for crash damage and Comprehensive Insurance Car for theft or weather damage. Personal injury protection focuses only on injury and medical expenses, not your vehicle.

You also need good liability insurance car to protect others you hurt. In some cases, Uninsured Motorist Coverage helps when the at‑fault driver has no insurance or too little. All these pieces together form Full Coverage Car Insurance for your budget and risk level.

PIP sits in the “people coverage” group, along with health insurance and disability insurance, so you’re not stuck paying big bills alone.

Comparison: PIP Coverage vs Other Options

Here’s a simple way to compare your choices for injury costs.

| Option | Cost (Typical Add‑On) | Time Needed To Pay | Effectiveness | Best For |

|---|---|---|---|---|

| Personal injury protection | 5–30 dollars/month extra | Days to weeks | High for short‑term medical expenses and lost wages | Drivers in no fault insurance or high medical cost states |

| MedPay (Medical Payments) | 3–15 dollars/month extra | Days to weeks | Medium, pays only medical bills | Drivers with solid income but basic health plans |

| Rely on health insurance only | 0 extra on auto | Weeks to months | Medium to high, but with deductibles | People with strong health and disability coverage |

| Sue with bodily injury claims | No extra premium | Months to years | High for serious injuries | Serious injury cases with clear at‑fault driver |

Data ranges based on average U.S. pricing from insurance industry surveys (2023–2024).

When You Might Need A Lawyer Or Attorney

Most people hope they’ll never need a lawyer, but sometimes it’s smart.

You might want an attorney if your PIP insurance claim gets delayed or denied, and your bills keep rising. You may also need help if you suffered serious injuries and need to know when you can step outside no fault insurance rules to sue.

In states like personal injury protection florida, personal injury protection michigan, ny, new york, texas, and nj, local laws are tricky. A good attorney understands the Florida personal injury protection statute or other local rules and can push back on unfair claim decisions.

Most personal injury lawyer offices offer free first talks and only get paid if they recover money for you, but always ask about fees clearly.

What To Avoid With Personal Injury Protection

Quick tip: a few common mistakes can really hurt your claim.

Don’t delay medical care after a crash, even if you think you’re fine. Delays can make your injury look less serious and can break rules like Florida’s 14‑day window for Florida personal injury protection insurance. Don’t ignore letters from your insurer asking for more info.

Don’t sign away rights or accept a quick settlement for PIP coverage or liability without understanding the long‑term impact. Once you sign, you often can’t ask for more later.

Don’t drop personal injury protection just to shave a few dollars off your premium if you have no health insurance or a big deductible. That small savings can become a big loss after one crash.

Do I Really Need Personal Injury Protection?

Here’s the thing: the answer depends on your state, health plan, and budget.

If you live in a no fault state like personal injury protection florida, ny, new york, nj, or personal injury protection michigan, you may have no choice because the law requires PIP insurance. In those places, your main decision is how high your PIP coverage limit should be.

If you’re in a state like texas, you ask: do I need personal injury protection if it’s optional? You look at your health insurance, savings, and risk tolerance. Drivers with weak health plans or unstable income usually benefit from keeping PIP.

You can review your whole policy, including Minimum Car Insurance Requirements, First Time Driver Insurance, and Best Car Insurance Companies to see which mix of coverages fits your life.

FAQ About Personal Injury Protection

A: PIP insurance is personal injury protection that pays medical expenses and sometimes lost wages after a crash, no matter who caused it.

A: Insurers in Texas must offer PIP insurance, but you can reject it in writing if you don’t want protection coverage Texas.

A: PIP insurance cost often adds about 5–30 dollars per month, depending on your state, limits, and risk level.

A: PIP coverage may pay lost wages, home help, and some passenger coverage, while health insurance usually only covers medical care.

A: Personal injury protection vs bodily injury: PIP covers you and your passengers; bodily injury liability covers people you injure in another car.

A: You might still want PIP because PIP insurance helps with lost wages and deductibles that health plans don’t pay.

A: The Florida personal injury protection statute requires at least 10,000 dollars of PIP and treatment within 14 days to unlock full benefits.

Conclusion

Here’s the thing: personal injury protection can be the difference between stress and stability after a crash.

You’ve seen how PIP coverage pays for medical expenses, lost wages, and passenger coverage in places like personal injury protection florida, personal injury protection michigan, ny, new york, texas, and nj. You’ve learned how PIP insurance compares to other coverages, what affects PIP insurance cost, and how personal injury protection vs bodily injury liability works. You also know when to call a lawyer or attorney and what mistakes to avoid.

Your next step is simple: pull out your auto policy or log into your account and check your PIP insurance limits today. If they’re low or missing, talk with your agent about raising them so your injury coverage actually matches your real life risks.

This article is for information only. Please consult a professional before making decisions.

🛡️ PIP Coverage Calculator

Calculate Your Personal Injury Protection Needs & Costs

📋 Coverage Breakdown

📊 PIP vs Other Options Comparison

| Coverage Type | Monthly Cost | Payment Speed | Best For |

|---|---|---|---|

| PIP Insurance | $5-30 | Days-Weeks | Fast medical + wages |

| MedPay Only | $3-15 | Days-Weeks | Medical bills only |

| Health Insurance | Varies | Weeks-Months | Comprehensive care |

| Bodily Injury Claim | $0 extra | Months-Years | Serious injuries |

Leave a Reply