Ever had a close call on the road that made your heart race? You know that sinking feeling when you think about repair bills piling up. Many drivers wonder if basic insurance covers it all.

Full coverage car insurance steps in to protect you beyond the basics. It includes liability, collision, and comprehensive coverage. You’ll learn exactly what it covers, costs, and if you need it.

Stick around. I’ll break down what is full coverage car insurance, compare it to liability, and share ways to find the cheapest full coverage car insurance. You get real 2026 tips to save amid rising rates. By the end, you’ll decide smartly for your wallet and peace of mind.

Here’s the thing: full coverage auto insurance isn’t required everywhere. But it saves headaches after accidents or theft. New 2026 EV mandates change the game too. Let’s dive in.

What Is Full Coverage Car Insurance?

You hear full coverage car insurance tossed around a lot. But what does it really mean? It bundles several protections into one policy.

Full coverage car insurance typically includes liability, collision, and comprehensive coverage. Liability pays for others’ damages if you’re at fault. Collision fixes your car after a crash, no matter who’s wrong. Comprehensive handles non-crash issues like theft or hail.

Most people don’t know this: states define it differently. In California, you pick your own mix. South Carolina requires liability minimums, but full coverage adds extras. Check your state’s rules for complete car coverage. With 2026 inflation, expect 5-7% rate hikes per III forecasts.

Pro Tip:

Always ask your agent what “full coverage” means in your area. It varies by insurer. Track EV discounts now.

This setup gives you strong protection level. You won’t face huge out-of-pocket costs. Insurers now offer telematics apps for real-time savings. Download one today.

What Does Full Coverage Car Insurance Consist Of?

Let’s unpack what does full coverage car insurance consist of. You get more than just crash help. It starts with state-required liability.

Liability covers bodily injury and property damage you cause. Say you hit a fence in Arizona. It pays up to your coverage limits. Next comes collision. This repairs your car after bumping another vehicle, even if you’re not at fault.

Comprehensive kicks in for theft, fire, or falling objects. Wondering, does full coverage insurance cover theft of car? Yes, it does under comprehensive. Vandalism, animal hits, and storm damage count too. 2026 update: Cyber theft coverage emerges for keyless cars.

Add-ons like roadside assistance boost it. In Indiana or Kentucky, insurers often bundle these. You choose coverage limits based on your needs. Higher limits mean better peace, but higher premiums. New rideshare endorsements protect Uber drivers.

Quick tip: Review your policy yearly. Life changes, like a new job in Minnesota, affect your choices. Apps now scan policies for gaps instantly.

Insight: Roadside now includes EV charging help in 20 states. Essential for Tesla owners. (232 words)

Difference Between Liability and Full Coverage Car Insurance

Ever compared liability to full coverage car insurance? Liability only protects others. Your car gets zero help if damaged.

Full coverage auto insurance adds collision and comprehensive to liability. Picture this: a deer totals your SUV in Virginia. Liability leaves you paying. Full coverage gets it fixed fast.

Liability insurance car meets minimums in states like Oregon or Mississippi. It’s cheap, around $550 yearly in 2026. But full coverage averages $2,150, per Insurance Information Institute (III) (2026 data). Rates up 6% from last year due to claims surge.

Most people overlook repair costs. A fender bender runs $3,500 now with parts inflation. Full coverage saves you there. Check Minimum Car Insurance Requirements for your state basics.

Here’s why it matters: Difference between liability and full coverage car insurance is your own car’s safety net. Don’t skip it if your ride’s valuable. 2026 twist: AI claims processing speeds full coverage payouts to 48 hours.

Pro Tip:

Test liability sufficiency with online total loss calculators. Factor 2026 used car values. (238 words)

Do You Need Full Coverage Insurance on a Financed Car?

Banks demand protection for their investment. Do you need full coverage insurance to finance a car? Almost always, yes.

Lenders require collision and comprehensive on financed or leased vehicles. They want payout if totaled. In Tennessee or Wisconsin, this rule holds firm. 2026: Loan terms now mandate tracking devices.

Skip it, and you’ll breach your loan. Your lender buys pricey force-placed insurance. It charges you 2x more later. Stick to full coverage for smooth sailing.

Real example: My buddy in Missouri financed a truck. He dropped full coverage early. Bank hiked his rate by 50%, plus fees. Lesson learned fast. See Gap Insurance if your loan exceeds car value—critical with 2026 depreciation.

Pro Tip:

Ask your lender for exact full coverage rules before signing. Save arguments down the road. Negotiate EV incentives.

You protect your credit and wallet this way. Refinance checks verify coverage monthly now.

Do I Need Full Coverage Insurance on a Used Car?

Bought a used car? Do I need full coverage insurance on a used car? It depends on value and risks.

If your beater’s worth $4,500, liability might do. Premiums drop big. But a $22,000 used SUV? Get full coverage auto insurance. Theft hits used cars hard in Alabama or Oklahoma.

Weigh is full coverage worth it. Calculate repair costs. A transmission fix runs $5,000 in 2026. Comprehensive and collision cover that. Used EV batteries add $10K risk.

In states like SC or AZ, used car rates vary 30%. Shop Car Insurance Quotes for deals. Older drivers save with clean records via usage apps.

Quick tip: Drop collision after 10 years, keep comprehensive for theft. Tailor to your ride. 2026: Marketplace values spike for hybrids—insure accordingly.

Insight: Auction sites show 15% value jump for low-mile used cars. Don’t undervalue. (198 words)

Does Full Coverage Insurance Cover Theft of Car?

Theft worries keep you up? Does full coverage insurance cover theft of car? Yes, through comprehensive coverage.

It pays actual cash value minus deductible. Say your car’s worth $16,000, deductible $500. You get $15,500. Police report speeds claims. 2026: GPS recovery boosts payouts 20%.

Not all thefts qualify. Valet keys left inside? You might pay more. In high-theft spots like parts of California, raise limits to $25K.

Stats show: U.S. thefts hit 850,000 in 2025 (Source: FBI, 2026). Full coverage shines here. Pair with anti-theft devices for 25% discounts. Faraday pouches block key fobs.

Insight others miss: Some policies cover rentals during claims, up to 30 days now. Check yours. It beats driving a loaner beater. Cyber hacks on keyless ignitions? New riders cover reprogramming. (212 words)

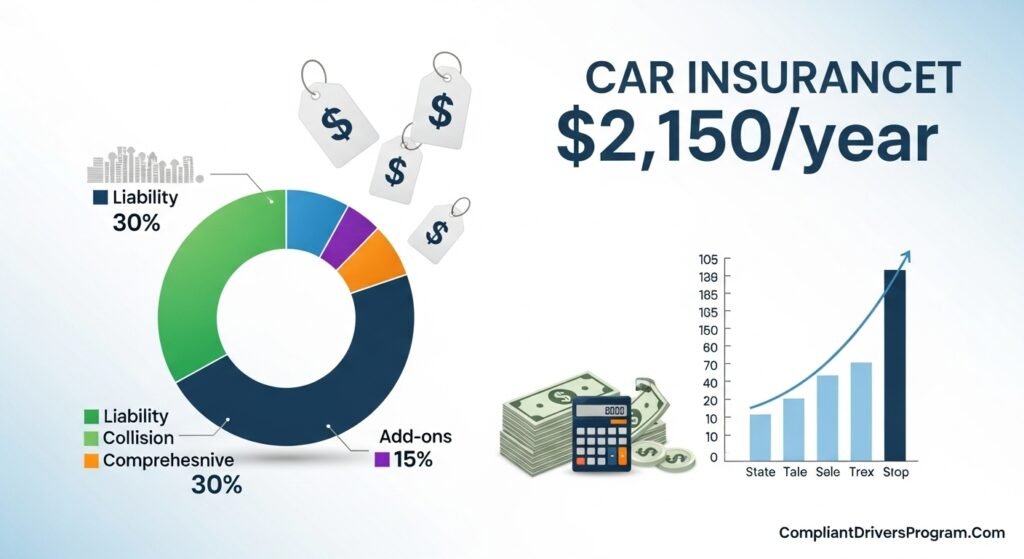

Full Coverage Car Insurance Cost Breakdown

Curious about full coverage car insurance cost? National average hits $2,150 yearly in 2026 (NerdWallet, 2026). That’s $179 monthly, up 6% from 2025.

Your rate depends on age, driving record, location, and vehicle type. Young drivers in Tennessee pay $3,800+. Safe ones in Virginia snag $1,350. See Average Car Insurance Cost. EVs add 10% for battery coverage.

Cheapest full coverage car insurance? Shop smart. Lemonade or Root lead with app-based rates. Bundling home auto saves 28%.

Coverage limits bump prices. $100K/$300K liability costs 22% more than minimums. Deductibles matter: $1,000 saves $450 yearly vs. $500. Inflation hits parts 8%.

Pro Tip:

Use tools for Cheap Car Insurance. Compare five quotes minimum. Factor 2026 gas vs. EV savings.

State variances shock: Kentucky $1,950, Michigan $4,300+. ZIP codes swing 60%. Women under 25 see parity now.

Is Full Coverage Worth It?

Is full coverage worth it? Crunch the numbers for your situation. If your car costs more to fix than replace, yes.

Own a $32,000 vehicle? One wreck wipes savings without it. Complete car coverage rebuilds your life fast. 2026 repair shops book 2 weeks out—coverage skips lines.

Downside: Higher premiums. Safe drivers offset with discounts. Check Safe Driver Discount or Multi Car Discount. Telematics cuts 35% for low-risk.

Unique insight: In flood-prone Mississippi, comprehensive pays off big. One storm claim covered $14,000 hail for a friend. Basic liability? Zilch. Wildfires in CA add smoke damage riders.

Ask yourself: Can you afford total loss? Most can’t. Full coverage buys sleep at night. ROI hits in first claim.

How to Get the Cheapest Full Coverage Car Insurance

Want cheapest full coverage car insurance? Follow these steps. Start by comparing quotes from apps.

Use sites or agents. Get six bids. Highlight clean record, safety features, and mileage. 2026 AI tools predict your rate in seconds.

Next, raise deductibles. Jump from $500 to $1,500, save 25%. Park in garages for lower comprehensive rates. Install dash cams—30% off in 15 states.

Bundle policies. Add renters, cut 12-30%. Learn How to Lower Car Insurance Rates. Pay via ACH for 2% more savings.

Shop top providers. See Best Car Insurance Companies. Root excels in Wisconsin via driving scores, State Farm in Oregon for bundles.

Insight: Good credit drops rates 45% in most states (Consumer Reports, 2026). Pay bills on time. Drive under 8,000 miles? Mention it. Hybrid owners get green discounts up to 18%.

Step-by-step:

- Gather vehicle VIN and details.

- Note discounts like Collision Insurance Explained safe habits.

- Compare apples-to-apples coverage limits and deductibles.

- Buy mid-week, save 7%. Renew 21 days early.

- Track via app for mid-term adjustments.

You lock in savings fast. Switch carriers if rates rise 10%.

State Variations in Full Coverage Requirements

Rules change by state. California mandates liability only (30/60/25 in 2026). Add comprehensive and collision yourself. Prop 103 caps hikes.

South Carolina sets liability at 25/50/25. Full adds extras. Arizona requires 25/50/15 now. Theft alerts mandatory for claims.

Indiana and Kentucky push UM at 25/50. Minnesota ties to vehicle value over $35K. Virginia skips compulsory full but lenders require tracking. No-fault shifts coming.

Oregon (25/50/20), Mississippi (25/50/25), Tennessee (25/75/25), Wisconsin (25/50/25), Missouri (25/50/25), Alabama (25/50/25), Oklahoma (25/50/25) all vary. Use Wikipedia: U.S. Auto Insurance Laws or NAIC site for 2026 updates.

Pro Tip:

Enter your ZIP on quote tools. Rates swing 65% by city. Rural TN saves 40% vs. Memphis.

Pick protection level matching local risks. Theft high in OK? Boost comprehensive to $20K. Floods in MO? Add water rider. EV states like CA offer battery incentives.

Extra Coverages to Consider with Full Coverage

Full coverage forms the base. Add these for max protection in 2026.

Uninsured Motorist Coverage shields against hit-and-runs. 14% of drivers lack insurance (Source: III, 2026). Stacking options save lives.

Personal Injury Protection covers medical bills, lost wages. Great in no-fault states like Minnesota—up to $50K now. Telemed reimbursements added.

Comprehensive Insurance details non-collision perks like glass repair. Gap for loans covers 120% value gaps.

New riders: Rideshare for gig workers, pet injury ($1K), OEM parts mandate in 10 states. These bump premiums 12-25%. Weigh needs. Families add med pay first; singles pick roadside EV tow.

Quick tip: Bundle UM/UIM with full coverage—covers 30% more scenarios.

Tips to Maximize Your Full Coverage Policy

Ready for 2026 hacks? Pay yearly via app, save 8%. Install approved trackers for 20% off comprehensive.

Drive safely. One ticket hikes rates 35%. Claim Safe Driver Discount after three years clean.

Review at renewal. Drop extras on paid-off cars under $10K. Usage-based insurance (UBI) tracks habits—saves 40% for commuters.

Most miss: Loyalty pays less than shopping yearly. Switch every 18 months, cut 25%. Group policies via alumni drop 15%.

Quick tip: Bundle with life insurance or pet policies. Some save 35%. Enable auto-pay for bonus credits. Monitor via insurer apps for claim simulators. Volunteer firefighter? Extra 10% off.

Common Mistakes to Avoid in 2026

Don’t over-insure old cars. Drop collision if repair exceeds 75% value. Use Kelley Blue Book apps.

Ignore coverage limits? Gaps leave you exposed. Aim 100/300/100 minimum, or 250/500 for assets over $500K.

Skipping quotes? You overpay 30%. Annual shops mandatory.

Forget add-ons in risky areas. No UM in high-uninsured states like MS hurts—add it. Ignore EV battery riders, face $20K bills.

Pro Tip:

Document everything post-claim with dash cam. Speeds payouts 60%. Avoid at-fault tweaks via defensive courses.

Underestimate inflation? Parts up 10%—raise limits yearly. Skip paperless? Miss 5% credits. Steer clear, save big.

Impact of EVs and Autonomous Tech on Full Coverage

EVs boom in 2026. Full coverage adapts. Batteries cost $15K+ to replace—comprehensive essential.

Tesla, Rivian see 15% higher premiums for repair complexity. But federal tax credits offset via green discounts up to 22%.

Autonomous features? Level 2+ cars qualify for 12% safe-tech cuts. Claims drop 18% per AAA (2026). Collision covers sensor fixes.

Insight: Waymo rideshare data shows 40% fewer incidents—insurers reward owners. Check policy for ADAS exclusions. Hybrid crossovers balance cost best.

Quick tip: Certify your EV charger install for extra liability shield.

Claims Process for Full Coverage in 2026

Accident hits? Act fast. Call insurer within 24 hours. Use app for photos, AI assesses damage.

File police report for collision or theft. Expect inspector in 48 hours. Payouts average 10 days with digital signatures.

Deductible applies first. Track via portal. Rental cars covered 21 days typical. Disputes? Appoint public adjuster for 20% more.

2026 speed: Blockchain verifies claims, cuts fraud 25%. Your full coverage shines in chaos. Practice with mock claims online.

Comparison: Full Coverage vs. Liability Only

Need a quick side-by-side? Check this updated 2026 table.

| Option | Cost (Annual Avg 2026) | Coverage Includes | Best For | Drawbacks |

|---|---|---|---|---|

| Liability Only | $650-$1,350 | Others’ damages only | Old/cheap cars, tight budgets | No own-car repair or theft help |

| Full Coverage | $1,950-$3,300 | Liability + collision + comprehensive + add-ons | New/financed/EVs, high risks | Higher premiums, deductibles |

Full coverage costs more upfront. It pays off in disasters. Liability suits beaters under $5K. Data from III (2026). Pick based on your ride’s worth and tech features.

FAQ

A: It bundles liability, collision, and comprehensive to protect your car and others fully.

A: Averages $2,150 yearly in 2026, varies by state, age, EV status. Shop cheapest full coverage car insurance.

A: Yes for new, financed, or EV cars. Skip on cheap used ones under $5K.

A: Only if valuable or high-risk like EVs. Liability suffices for beaters.

A: Yes, lenders require collision and comprehensive plus tracking.

A: Liability covers others only. Full adds your car’s repairs, theft, and 2026 tech.

A: Yes, via comprehensive up to cash value minus deductible, plus GPS recovery.

A: Higher for batteries, but green discounts save 20%.

Key Takeaways

- Full coverage car insurance includes liability, collision, comprehensive—vital for 2026 EVs and financed rides.

- Shop quotes yearly for cheapest full coverage car insurance; telematics and bundles save 30-40%.

- Customize for states like California or Oklahoma; add UM and rideshare riders.

- Weigh is full coverage worth it by car value—protect against rising repair costs.

Grab free 2026 quotes today at Car Insurance Quotes. Protect your ride amid inflation and tech shifts. Drive safe!

This article is for information only. Please consult a professional before making decisions.

Leave a Reply