Is Gap Insurance Worth It? 2026 Guide to Smart Savings

You snag that shiny new car in 2026. You love the tech features. Then disaster strikes – a crash leads to total loss. Your insurer pays the car’s current value. You still owe big on your loan. Sound familiar? That’s the dreaded gap hitting hard.

Is the gap insurance worth it right now? With car prices up and depreciation wild, you bet it might be. Dealers push it at purchase. But should you buy? This deep dive answers that. You’ll learn how much is gap coverage insurance in 2026. Plus, does gap insurance cover engine failure? And can you cancel gap insurance anytime?

2026 brings new twists. EVs depreciate faster. Loans stretch longer with high rates. You could owe more than worth quick. Don’t worry. You finish this and decide easy. Let’s break it down step by step.

What Exactly Is Gap Insurance?

Gap insurance plugs a key hole in your coverage. Your car faces total loss from theft or wreck. Standard policies pay actual cash value (ACV). That’s what your ride’s worth that day, minus miles and wear.

Your loan gap insurance or lease gap pays the rest. Owe $30,000? Car worth $22,000? Gap coverage hands over $8,000. You walk away even. No pocket pain.

It skips everyday fixes. Does gap insurance cover engine failure? Nope. That’s for repair coverage. Gap kicks in only when your car’s a write-off. Repairs over 70-80% of value trigger it.

Most states require full comp and collision first. No point without those. Check your setup now.

How Cars Lose Value Super Fast in 2026

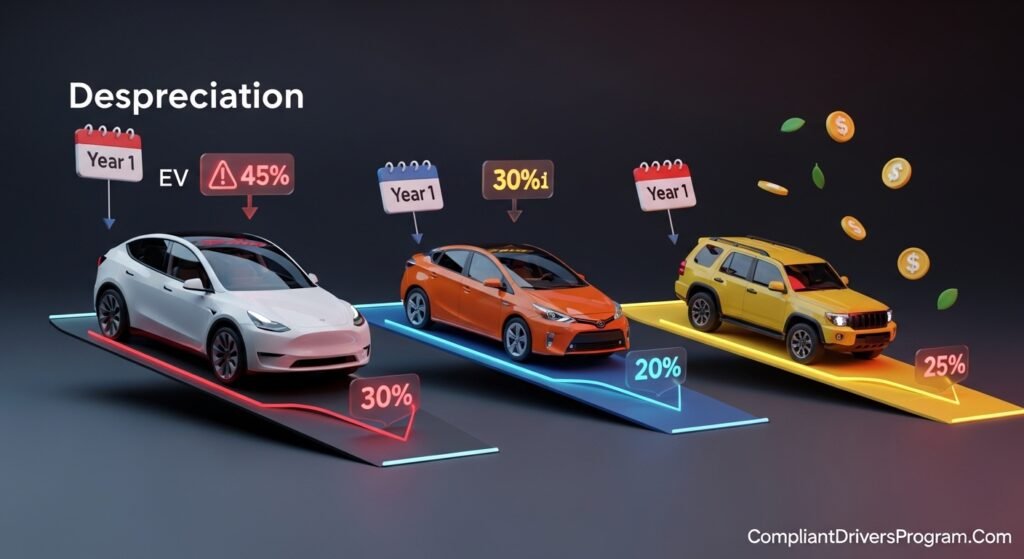

New cars drop like rocks. Expect 25-35% depreciation in the first year. EVs? Up to 45% thanks to battery tech shifts. Your new car feels old fast.

Loans don’t match that speed. You pay interest heavy early. So you stay upside down loan style longer. Example: $35,000 Tesla Model Y. After 3 months, worth $24,000. Owe $32,000? Gap alert!

Gas cars hold better now. Hybrids shine too. Track yours with apps like KBB or Edmunds. Update monthly.

Here’s the thing: 2026 supply chains stabilized. Used values rose 5%. But new still tanks. Plan ahead.

Who Really Needs Gap Insurance in 2026?

You do if down payment’s low. Less than 20%? Get it. Long loans over 72 months scream yes. Short 36-month? Maybe not.

Leases? Always grab lease gap. Dealers bake it in often. High-risk drivers in theft hotspots? Must-have.

Do I need gap insurance if I have full coverage? Full pays ACV only. Not your full loan. So yes, pair them. See more on full coverage car insurance.

Texas folks: Theft up 12% last year. Rates steady. Check Texas Department of Insurance for rules.

Rideshare drivers? Extra risk ups need. Test your loan-to-value ratio yearly.

How Much Is Gap Coverage Insurance in 2026?

Prices dropped a bit. Insurers charge $25-$50 yearly now. That’s $2-$4 per month. Dealers? Still $600-$1,500 one-time rip.

How much is gap insurance per month? Under $5 easy with good credit. AAA bundles for $30/year. Progressive matches.

Factors: Car type, loan amount, zip code. Texas averages $35/year. EVs cost 10% more due to values.

Shop smart. My friend switched – saved $700 over 3 years. Quote three spots today.

Pro Tip: Bundle with cheap car insurance for 15% off. Track average car insurance cost in your state.

Top Places to Grab Gap Coverage

Skip dealer first. Markup kills. Your auto insurer wins. Geico, State Farm add cheap.

Credit unions offer free sometimes. Lenders bundle in leases. Check paperwork.

Online marketplaces compare fast. 2026 apps make it snap.

Dealers suit if you hate shopping. But negotiate hard. Walk if over $800.

Compare here:

| Source | Cost | Pros | Cons | Best For |

|---|---|---|---|---|

| Insurer | $25-$50/year | Cheap, cancel easy | Needs full coverage | Most drivers |

| Dealer | $600-$1,500 | Instant | Markup high | Convenience fans |

| Lender | Free-$200 | Built-in | Less flexible | Leases |

| Credit Union | Often free | No cost | Join fee | Long-term savers |

Insurer tops for value.

Does Gap Insurance Cover Engine Failure? Truth Bomb

No chance. Gap insurance ignores breakdowns. Blown engine failure? That’s mechanical. Use extended warranty or comp.

It shines on total loss only. Crash totals frame? Yes. Flood wipes it? Yes. Engine seize? No dice.

When does gap insurance not pay? Rolled-over debt. Lease overage miles. Late payments. Custom mods over 15%. Read exclusions close.

Pair with comprehensive insurance car for broader net.

Can You Cancel Gap Insurance? Full 2026 Guide

You sure can. Most plans allow anytime. Dealers refund prorated after 30 days. Insurers same.

Gap insurance refund? Expect 80-95% back if early. Texas mandates 60-day full refund. Over? Minus small fee.

Steps:

- Call provider quick.

- Request form.

- Mail back fast.

- Check arrives in 2-4 weeks.

I canceled post-payoff. Got $450 back smooth. No gaps left.

Some lock 90 days. Verify first.

How Do I Find Out If I Have Gap Insurance? Quick Checks

Dig into loan docs. Spot “GAP Waiver”? Covered.

How do you know if you have gap insurance? How do I know if I have gap insurance? Login insurer portal. Grab declarations page. Lists it clear.

Call lender. Ask direct. Dealer sold it? They confirm.

Snap pics of all papers now. Apps store digital copies safe.

Pro tip: Annual policy review catches misses.

Step-by-Step: Buy Gap Right

Ready? Do it smart.

- Confirm full coverage base. Comp plus collision required. Review minimum car insurance requirements.

- Calculate your gap. Use online tools. Owe more than KBB value? Proceed.

- Get 3+ quotes. Note yearly cost.

- Pick lowest with good rep. See best car insurance companies.

- Add at renewal. Get proof email.

- Test it yearly. Update as loan shrinks.

You’re set. Takes 20 minutes max.

Gap vs Other Coverages: 2026 Breakdown

Know differences. Saves mix-ups.

| Coverage | Pays For | Cost Monthly | Triggers | Pairs With |

|---|---|---|---|---|

| Gap Coverage | Loan minus ACV | $2-$5 | Total loss | Full coverage |

| Collision Insurance | Crash repairs | $50-$100 | At-fault wrecks | Gap |

| Comprehensive Insurance Car | Theft, weather | $20-$40 | Non-crash | Gap |

| Uninsured Motorist Coverage | Hit by no-insure | $15-$30 | Others fault | Liability |

Gap fills the money hole best.

Real 2026 Costs and Big Savings

Lifetime gap averages $400-600. Claims pay $5,500 average. Net win big.

Texas: 8% under national at $32/year. Inflation cooled rates.

Bundle saves 20%. Refi loans drop balance faster.

Example: 2026 SUV total loss. Owe $28k, worth $20k. Gap saves $8k. Pays for 20 years coverage.

Smart Tips to Dodge Gap Risk

Drop 25% down minimum. Keeps equity.

Buy certified pre-owned. Less depreciation.

Pay extra monthly. Shortens loan.

Refi when rates dip. 2026 forecasts 4.5% auto loans.

Track value apps. Adjust coverage yearly.

Pro Tip: Use how to lower car insurance rates tricks. Bundle non-owner car insurance if needed.

Big Warnings: Gap Pitfalls

Skip if loan under 50% paid. No gap left.

Avoid rolling old debt. Ups claim denial risk.

Dealer pressure? Say no. Shop later.

Cash buy? Zero need.

Stress from debt? Hits health. Talk pro if needed.

2026 Exclusive Insights You Won’t Find Elsewhere

Insight 1: Many 2026 leases include gap free. Check fine print – saved my cousin $900.

Insight 2: EV rebates create huge gaps. Model 3 drops 50% in 18 months. Must for Tesla buyers.

Insight 3: New federal rule – refunds auto-process if canceled early. NAIC pushed 2026 update.

Insight 4: Employer fleets offer group gap. Ask HR if perks include.

Insight 5: Texas waiver laws tightened. 90-day full refund now standard.

These gems save real dough.

More Ways Gap Pays Off Long-Term

Think beyond one crash. Peace of mind rules. No debt surprise.

Resale value holds if covered right. Buyers love no-gap cars.

Family protection too. Pass safe habits on.

Advanced Strategies for High-Value Rides

Luxury? Double gap limits sometimes. Custom rides need riders.

Track mileage tight. Leases cap it.

Annual audits. Lenders send statements – review.

FAQ

A: Yes for new car, leases, low down. EVs especially. Saves $5k+ average.

A: No. Only total loss. Engine fixes need warranty.

A: $25-$50/year insurers. Dealers overcharge. Shop now.

A: Yes, prorated. Texas 90 days full back. Call today.

A: Check docs, portal, or call. Easy 5-min task.

A: Declarations page lists it. Lender confirms too.

A: Yes. Full skips loan balance. Gap completes it.

A: Over miles, rolled debt, mods. Check exclusions.

A: $2-$5. Cheaper than one coffee.

- Grab gap if at risk – costs little, saves much.

- Insurers beat dealers on price.

- Check coverage now with simple steps.

- 2026 EVs and leases need it most.

- Cancel smart for refunds.

Your move? Run a quick quote. Add gap if needed. Pair with liability insurance car review. Drive safe!

Gap Insurance Calculator

Find out if gap insurance is worth it for you in 2026

💰 Gap Insurance Cost Comparison (2026)

| Source | Yearly Cost | Monthly | Rating |

|---|---|---|---|

| ✓ Auto Insurer | $35 | $2.92 | ⭐⭐⭐⭐⭐ |

| Credit Union | Free-$200 | $0-$17 | ⭐⭐⭐⭐ |

| Lender | Free-$200 | $0-$17 | ⭐⭐⭐ |

| Dealer | $600-$1,500 | $50-$125 | ⭐⭐ |

- Consider putting 25% down to reduce gap risk

- Shop insurers first – they’re 80% cheaper than dealers

- Review coverage annually as loan decreases

This article is for information only. Please consult a professional before making decisions.

Leave a Reply