Ever hit a bump while driving for Uber and wondered if your insurance covers it? You start the app, pick up riders, and suddenly face big coverage gaps. Most drivers don’t know their personal policy leaves them exposed.

That’s why you need this complete guide on Uber Lyft insurance. You’ll learn the three key periods, what rideshare gap coverage fixes, and real costs for 2026. By the end, you’ll know exactly how to protect your car and wallet. Let’s dive in and keep you safe on every ride.

What is Uber Lyft Insurance?

Uber Lyft insurance means protection for drivers like you who use rideshare apps. It covers accidents during app use, but not all times match your regular car insurance. Apps like Uber and Lyft add their own layers on top of your policy.

Here’s the thing: Your personal policy often skips business rides. That leaves you paying out of pocket for crashes. Rideshare insurance steps in to fill that hole.

Think of it like this. You drive to work fine, but turn on the app and rules change. You need extra coverage to stay safe.

Why Rideshare Insurance Matters

Driving for Uber or Lyft boosts your income fast. But one crash can wipe out your earnings. Standard auto insurance skips rideshare work, so you face huge bills alone.

Rideshare gap coverage keeps your finances safe. It pays for repairs, medical bills, and lawsuits you can’t handle. Most people don’t know this, but claims skyrocket without it.

You’ll sleep better knowing passengers and your car stay protected. Skip it, and you risk everything you’ve built.

The Three Coverage Periods Explained

Uber and Lyft split coverage into three periods. Each one changes what protects you. Know these to avoid shocks.

Period 1: App on, waiting for rides. Uber gives $50,000 per person for injury, $100,000 per crash, and $25,000 for damage. Collision skips this phase mostly.

Period 2: You accept a ride, head to pickup. Now you get up to $1 million liability plus some collision help. Your car gets basic protection here.

Period 3: Passenger inside, full trip. Best coverage kicks in with $1 million liability and full collision. This matches big risks you face.

Quick tip: Always check your state’s rules. Coverage varies a bit by location.

Uber Driver Insurance Breakdown

Uber sets clear rules for your protection. They require your own auto insurance for Uber and Lyft drivers first. Then they layer on theirs when logged in.

Uber’s Period 1 stays thin at $50/100/25K limits. You might pay deductibles up to $2,500 if your policy denies. Uber driver insurance shines in Periods 2 and 3 with $1M coverage.

Most drivers add rideshare insurance from State Farm or Geico. It costs $15-30 extra monthly. Don’t skip this or face claim denials.

Pro Tip:

Log your miles before and after rides. This proves personal use if insurers question you.

Lyft Driver Coverage Details

Lyft works much like Uber but with small twists. You need car insurance for Uber and Lyft drivers that meets state minimums. Lyft adds $50K/$100K/$25K in Period 1 if needed.

Lyft driver coverage jumps to $1M liability once en route. They cover passengers well but limit vehicle damage early. Add your own policy for full peace.

Lyft pushes Express Drive rentals with built-in insurance. You pay $200-300 weekly, but it skips gaps. Weigh this against owning your car.

Rideshare Gap Coverage Explained

Ever hear of rideshare gap? It’s the hole between your personal policy and app coverage. Your insurer drops you during app time, apps don’t fully step up.

Rideshare gap policies from Allstate or Progressive fix this. They add liability and collision for all periods. Costs run $20-40 per month based on your car.

Without it, a fender bender costs you $5,000 easy. Get quotes yearly to match your miles.

Do Uber Drivers Need Special Insurance?

Yes, do Uber drivers need special insurance? Your regular policy likely excludes rideshare. Insurers like USAA deny claims if they find app use.

You need rideshare insurance on top. It stamps your policy as rideshare-friendly. Skip it and lose protection mid-trip.

Check your declaration page. Look for “excludes livery or rideshare.” If there, upgrade now.

Personal Policy vs Commercial Coverage

Your personal policy works off-app only. It covers grocery runs or family trips fine. But rideshare counts as business use.

Commercial coverage treats you like a taxi driver. It costs more at $150-300 monthly. Use it if you drive 40+ hours weekly.

Most part-timers stick with personal plus rideshare gap. Save money without skimping safety. Compare both for your needs.

| Coverage Type | Cost Per Month | Best For | Limits | App Time Coverage |

|---|---|---|---|---|

| Personal Policy | $80-150 | Off-app drives | State minimums | None |

| Rideshare Add-on | +$15-40 | Part-time drivers | Matches app | All periods |

| Commercial Coverage | $150-300 | Full-time pros | Higher limits | Full time |

| TNC Insurance | $100-250 | Heavy Uber/Lyft use | $1M liability | Gaps filled |

Rideshare Insurance Cost Breakdown

Worried about rideshare insurance cost? It adds $180-500 yearly to your bill. Your location, car age, and miles drive the price.

New drivers pay less at $15/month extra. High-mile folks hit $40. Shop Geico or Allstate for deals.

Pro tip: Bundle with home insurance. Save 10-20% right away. Track your 15,000 personal miles yearly for accurate quotes.

Ready to see your numbers? Use our Rideshare Insurance Calculator right here. Plug in your details for instant quotes on mileage-based insurance Uber Lyft personal use 15000 miles/year quotes. It factors your state, car, and driving habits.

Rideshare Insurance Calculator

Get your personalized Uber & Lyft insurance cost estimate in 60 seconds

Driver Profile

Select your rideshare platform & schedule

Vehicle Details

Your car info affects coverage costs

Current Insurance

Your existing coverage details

Coverage Preferences

Choose your desired protection level

⚠️ This calculator provides estimates only. Actual premiums depend on your insurer, credit, claims history, and state regulations. Consult a licensed insurance agent for accurate quotes. Rates shown are for 2025-2026 averages.

Best Insurance for Uber Drivers

What’s the best insurance for Uber drivers? State Farm leads with flexible rideshare insurance. They cover gaps cheap and fast.

Progressive follows close with app endorsements. Geico suits budget folks at low rates. Pick based on your claims history.

Test drive quotes from three. Look for $1M umbrella too. That extra shield costs $200/year but saves millions.

Does Uber or Lyft Offer Health Insurance?

Does Uber or Lyft offer health insurance? No, they skip full plans. Drivers qualify for subsidies if over 1,000 rides quarterly.

Uber had a basic plan pre-2025, but it ended. Lyft pushes marketplace options now. You buy your own through healthcare.gov.

Get occupational accident coverage instead. It pays medical for work injuries at $10K limits.

Commercial Auto Options for Heavy Drivers

Full-time? Grab commercial coverage. It handles unlimited rideshare without exclusions. Link to our Commercial Vehicle Insurance guide for details.

Costs hit $2,000 yearly but cover fleets too. See Commercial Fleet Insurance if you scale up. Perfect for pros.

Compare with Commercial Auto Insurance Cost page next.

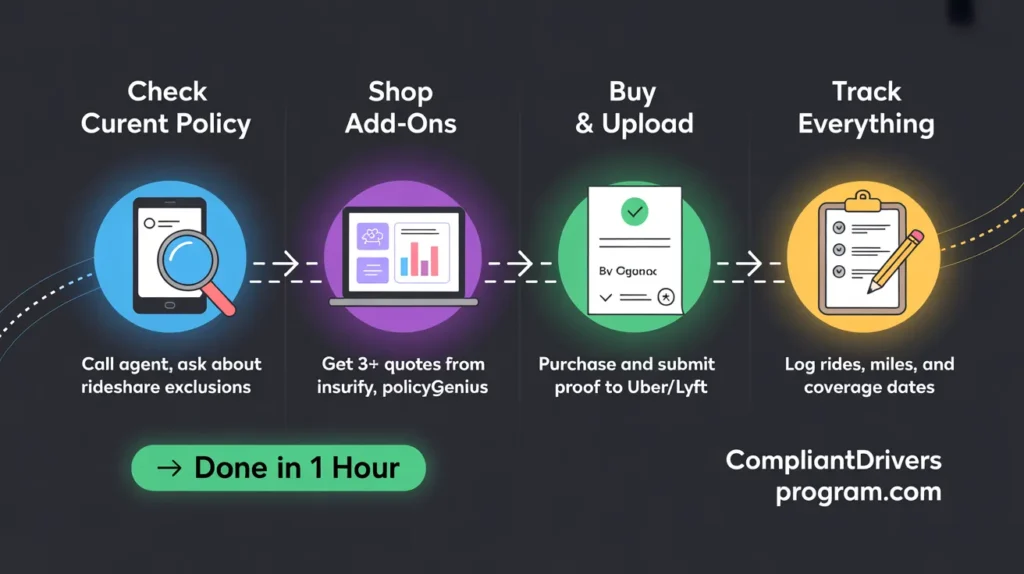

Step-by-Step: How to Get Rideshare Insurance

Ready to insure right? Follow these steps.

First, check your current policy. Call your agent and ask about rideshare.

Second, shop add-ons. Use sites like Insurify for three quotes fast.

Third, buy and update Uber/Lyft. Upload proof to stay active.

Fourth, track everything. Log rides to prove coverage needs.

Done in one hour. You’re set for safe drives.

Tips for Better Rideshare Coverage

Drive safe to cut premiums 20%. Avoid night rides if new.

Install dash cams. Insurers love proof and drop rates.

Bundle policies. Add renters for extra savings.

Link to Delivery Driver Insurance if you multi-app.

What to Avoid with Uber Lyft Insurance

Don’t hide rideshare from your insurer. Claims get denied fast.

Skip cheap out-of-state policies. They fail local crashes.

Ignore state minimums. Fines hit $500 plus gaps.

Never drive without app-off coverage. Always have basics.

Cost and Time Expectations

Expect $300-800 yearly total. Setup takes 30 minutes online.

Claims process runs 2-4 weeks. Faster with dash cam proof.

Shop yearly. Rates drop as you build safe history.

Warnings and Common Mistakes

Most miss Period 1 gaps. Add collision there.

Don’t max personal miles. Over 15K triggers commercial needs.

Forget passenger lawsuits. Get $1M limits minimum.

FAQ

A: Yes. Regular policies exclude rideshare. Add rideshare insurance for full protection.

A: State Farm or Progressive. They offer cheap gap coverage tailored to rideshare.

A: No full plans. Buy your own or use their accident coverage.

A: Expect $250-450 yearly add-on. Use our Rideshare Insurance Calculator for your quote.

Conclusion

You now know Uber Lyft insurance inside out. Key points stick with you.

- Cover all three periods with rideshare insurance add-ons.

- Budget $20-40 monthly to close rideshare gap risks.

- Shop State Farm or Geico for best rates.

- Use our [Rideshare Insurance Calculator] for personalized mileage-based insurance Uber Lyft personal use 15000 miles/year quotes.

Your next step? Get a quote today. Protect your rides and income now. Safe driving!

This article is for information only. Please consult a professional before making decisions.

Leave a Reply